While you debate salary vs. dividends, a parallel silent decision could tilt the scale by thousands of dollars.

Mark is a dentist in Mississauga. His practice bills around $650,000 a year. Last year, after a conversation with his accountant, he made what seemed like the obvious choice: he bought his new SUV, $62,000 before tax, in his corporation’s name. “It’s a write-off,” he was told. He drives about 22,000 km a year, two-thirds of it for work. It all made sense.

Six months later, while preparing his returns, his accountant dropped a sentence Mark hasn’t forgotten: “You know, with your driving pattern, you might’ve been better off keeping the car in your personal name and getting a tax-free allowance. We’re talking five-figure annual difference.”

Five figures. In a car. Per year.

The variable everyone forgets

When an incorporated professional sits down to plan their compensation, the debate almost always comes down to the same question: salary or dividends? Outcome: the spreadsheets, the integration math, the CPP cost, and the RRSP room calculation. Hours spent optimizing, sometimes, a few thousand dollars’ difference in net income.

Meanwhile, another decision sits quietly at the bottom of the file: how the business treats the owner’s vehicle. It’s rarely framed as a tax optimization question. It’s an operational decision, made once, never revisited.

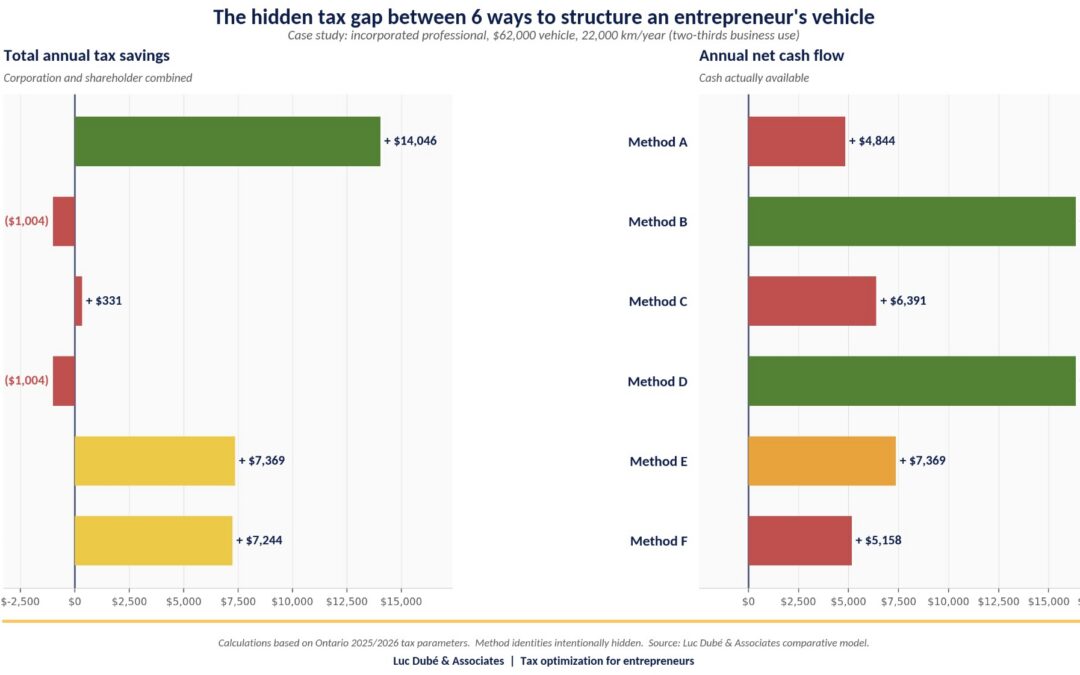

Based on our comparative modeling of real client files, the annual tax gap between the best and worst way to structure an entrepreneur’s vehicle regularly exceeds $10,000, and reaches $15,000 or more in many cases. For most incorporated business owners, that gap is bigger than the difference between paying yourself in salary or dividends.

Which changes the whole conversation.

Why does nobody see it?

Three reasons. First, the calculation is complex. It crosses six distinct tax regimes: kilometric allowance, corporate purchase, corporate lease, conditional sale agreement, personal motor vehicle deduction under s. 8(1)(h.1) ITA, and expense reimbursement. Each has its own rules on taxable benefits, capital cost allowance ceilings, and standby charges. Nobody handles any of these casually.

Second, the decision is made at the wrong moment. When the owner buys the car, they’re thinking of delivery, financing, and sales tax. Not annual tax optimization. The tax advisor arrives later. Too late to restructure.

Third, and most counterintuitive: the “best” answer depends on three specific variables that few advisors take the time to evaluate together. The percentage of business use, the vehicle’s cost, and the holding horizon. Change just one, and a regime can move from first to last place.

Three questions that decide everything

Before signing anything, here are the three questions to ask. Not the other way around.

- How many business kilometers, really? The critical threshold sits around 50% of total use. Below it, some regimes become tax-punishing. Above it, other mechanisms open up, notably the reduced standby charge, which can halve or quarter the taxable benefit. Without a CRA-compliant logbook, none of this is defensible.

- How much does the vehicle actually cost? The CRA imposes a cap on capital cost allowance: $38,000 before tax for 2026 vehicles, roughly $42,940 with HST in Ontario. Beyond that, every additional dollar generates zero corporate tax savings. At $65,000, a corporate purchase loses much of its appeal. Leasing operates under a different ceiling, $1,050 per month plus tax.

- How long are you really keeping it? The horizon flips the verdict. Five years or more: ownership wins back. Three or four years: leasing captures more cost. Conditional sale sits in a hybrid zone. The wrong choice on this one variable alone can erase thousands in annual optimization.

The decision order is backward

Here’s where the trouble starts. Most entrepreneurs make these decisions in this order: first buy the car, then figure out where to park it tax-wise, then optimize the rest of their compensation. The car becomes an immutable input.

The right order is the opposite. First project use and holding horizon, then model the six regimes, then integrate the verdict into the overall compensation plan. Only at that point does the salary-versus-dividends debate make full sense, because you know how much money you’ve already secured before walking into it.

And Mark?

Mark didn’t lose his car. But he lost six months and likely more than $8,000 in tax efficiency he won’t recover on this vehicle. Over five years, that gap could’ve nearly financed a replacement.

The worst part isn’t the mistake. It’s that one hour of analysis, at the right moment, that would have prevented it. Before signing the bill of sale. Before deciding on annual compensation. Before debating salary versus dividends.

Next time you plan your compensation, don’t start with the usual question. Start with this one: where does my vehicle fit into the equation? The hidden tax gap there can reshape your entire pay strategy.

At Luc Dubé & Associates, we’ve developed a comparative model that runs all six automotive tax regimes against your real profile. One hour of analysis can reveal a five-figure gap. Book a consultation to find out what’s hiding in yours.