A tax-free, leveraged bet on land has outcompeted productive investment and reshaped the economy.

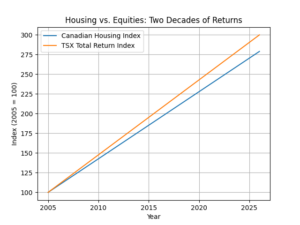

At first glance, the numbers tell a simple story: in 2005, the average Canadian home sold for approximately $230,000; by early 2026, that figure had climbed to roughly $660,000 (Canadian Real Estate Association, MLS® data). This is not merely appreciation; it reflects a deeper reallocation of how wealth is generated in Canada. Over nearly two decades, housing has delivered returns that resemble those of equity markets; however, the more uncomfortable truth is not that housing performed well, but that it was structurally positioned to do so.

That comparison, however, requires an important clarification: the TSX appears to outperform housing in Chart 1 because it reflects total returns, including reinvested dividends, whereas housing is measured primarily through price appreciation. A true price-to-price comparison significantly narrows the gap. The key takeaway, therefore, is not that stocks outperform housing but that housing, despite producing no income or economic output, has delivered returns comparable to those of equities.

As shown in Chart 1, while long-term performance may converge, the underlying drivers of those returns are fundamentally different, and it is precisely this difference that matters. A company grows because it produces goods, services, or innovation; a house appreciates because supply is constrained where demand is strongest, and because capital has been systematically directed toward it over time. Low interest rates, restrictive zoning, and demographic pressures all contribute to this dynamic; however, the most powerful force is fiscal. In Canada, housing is not merely an asset class; it is a tax-advantaged strategy.

As shown in Chart 1, while long-term performance may converge, the underlying drivers of those returns are fundamentally different, and it is precisely this difference that matters. A company grows because it produces goods, services, or innovation; a house appreciates because supply is constrained where demand is strongest, and because capital has been systematically directed toward it over time. Low interest rates, restrictive zoning, and demographic pressures all contribute to this dynamic; however, the most powerful force is fiscal. In Canada, housing is not merely an asset class; it is a tax-advantaged strategy.

At the center of this system sits a rarely debated policy lever: the principal residence exemption. In practical terms, it functions as follows: under the Income Tax Act, capital gains realized on the disposition of a qualifying principal residence may be fully exempt from taxation, subject to designation rules and conditions. While no explicit monetary cap applies, the exemption is limited to the designated number of years and restricted to one property per family unit. As a result, large gains can often be realized tax-free under the appropriate conditions. The Department of Finance estimates the annual fiscal cost of this measure at approximately $5 to $6 billion, making it one of the largest tax expenditures in Canada. Although politically sensitive and rarely reformed, the exemption has been indirectly constrained in recent years through measures such as anti-flipping rules and enhanced reporting requirements.

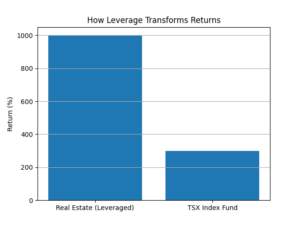

When combined with leverage, the effects are amplified dramatically: a $60,000 down payment on a $300,000 home in 2005 could now correspond to a property worth approximately $900,000, generating a $600,000 gain. This represents a tenfold return on invested capital, entirely sheltered from taxation under Canada’s principal residence rules. By contrast, an equivalent $60,000 investment in the TSX, with dividends reinvested, would have grown to approximately $170,000 to $230,000 over the same period, depending on market timing and return assumptions. These gains, unlike housing, would be partially taxable upon realization.

As illustrated in Chart 2, the amplification of gains, combined with tax-free treatment in Canada, helps explain why real estate has become a dominant wealth-building strategy for households. This is not a perfect apples-to-apples comparison, and that is precisely the point: while both real estate and equities can be leveraged, the nature of that leverage is fundamentally different. In housing, leverage is widely accessible, relatively low-cost, and supported by long-term financing structures such as mortgages, often with limited interim repricing risk. In contrast, leverage in equity markets typically involves margin borrowing or derivatives, which are more expensive, more volatile, and subject to margin calls, making them far less commonly used by households as a long-term strategy.

As illustrated in Chart 2, the amplification of gains, combined with tax-free treatment in Canada, helps explain why real estate has become a dominant wealth-building strategy for households. This is not a perfect apples-to-apples comparison, and that is precisely the point: while both real estate and equities can be leveraged, the nature of that leverage is fundamentally different. In housing, leverage is widely accessible, relatively low-cost, and supported by long-term financing structures such as mortgages, often with limited interim repricing risk. In contrast, leverage in equity markets typically involves margin borrowing or derivatives, which are more expensive, more volatile, and subject to margin calls, making them far less commonly used by households as a long-term strategy.

As a result, housing has evolved from shelter into strategy: over time, it has become a retirement plan, a primary wealth-building vehicle, and a leveraged investment structure embedded in household financial planning. The behavioral response is entirely rational: buy early, borrow as much as possible, and hold. This is not speculation; it is incentive alignment. Canadians did not collectively decide to treat housing like a stock; policy nudged them in that direction.

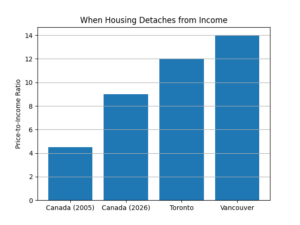

The consequences are now evident in the data: the median income in Canada was approximately $74,000 in 2023 (Statistics Canada), while the average home price now exceeds $660,000. This implies a national price-to-income ratio approaching nine, with major urban centers far exceeding that level (National Bank of Canada, Housing Affordability Monitor, 2025). Research from the OECD confirms that tax systems that fully exempt housing gains tend to distort capital allocation and contribute to upward pressure on prices (OECD, Housing Taxation in OECD Countries, 2022). Similarly, CMHC has noted that Canadian households are increasingly incentivized to rely on housing gains for wealth accumulation, reinforcing generational inequality (CMHC, Wealth and Generational Inequity in Canadian Housing).

As shown in Chart 3, this growing gap reflects structural affordability pressures and signals a market driven more by capital dynamics than by underlying income growth. This dynamic creates a self-reinforcing cycle: rising prices generate tax-free gains; those gains attract more capital; increased demand pushes prices higher still. The system feeds itself. This is not market dysfunction; it is the predictable outcome of the policy framework in place.

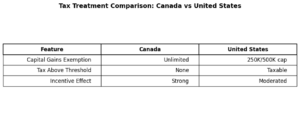

A comparison with the United States further clarifies Canada’s distinctive approach: under U.S. tax law, capital gains on a principal residence are taxable by default, though up to $250,000 for individuals and $500,000 for married couples can be excluded (Internal Revenue Code, 26 U.S.C. §§ 61, 1001, 121; Treasury Regulations §§ 1.121-1, 1.121-2). Any gain above these limits is taxed. This mechanism imposes a ceiling on tax-free accumulation and limits the extent to which housing can serve solely as an investment vehicle. Canada’s principal residence exemption, while subject to conditions, effectively allows qualifying gains to be realized tax-free, meaning the marginal dollar of gain can often escape taxation entirely.

As illustrated in Chart 4, Canada’s tax framework provides stronger encouragement for capital allocation into housing and contributes to higher price sensitivity. The broader implication extends beyond housing itself: when the most attractive investment in an economy is leveraged, tax-favored, and non-productive, capital will flow toward it. This means less capital directed toward businesses, innovation, and productivity, and more capital tied up in land and existing housing stock. Over time, this alters the structure of the economy itself. Canada increasingly risks becoming a place where wealth is built not by creating value, but by owning assets early.

For those who entered the market at the right time, the system has worked extraordinarily well; however, for new entrants, the equation is fundamentally different: higher prices, lower expected future returns, and increased exposure to interest rate fluctuations define today’s market. The question is no longer whether housing has behaved like a stock; it is whether Canada can sustain an economy in which the most reliable path to wealth has been ownership rather than production.

Ultimately, the conclusion is difficult to avoid: Canada did not stumble into a housing market that behaves like an equity market; it built one, through a combination of tax policy, financial leverage, and structural constraints. To realign housing with its intended social and economic role, policymakers, citizens, and industry leaders must actively reconsider these incentives and engage in substantive dialogue on reform. Unless these efforts are made, housing will continue to function not primarily as shelter, but as the country’s most powerful financial asset.

Disclaimer: This analysis is restricted to the principal residence regime under the Income Tax Act. It does not examine the tax implications applicable to real estate acquired or held for investment, rental, or business purposes.