In Canada, the ones paying the least tax in retirement are those who have nothing and those who have everything. Between the two: the careful saver, the worker who listened to his banker, the Brian who maxed out his RRSP for forty years. He pays the full marginal rate for both of them.

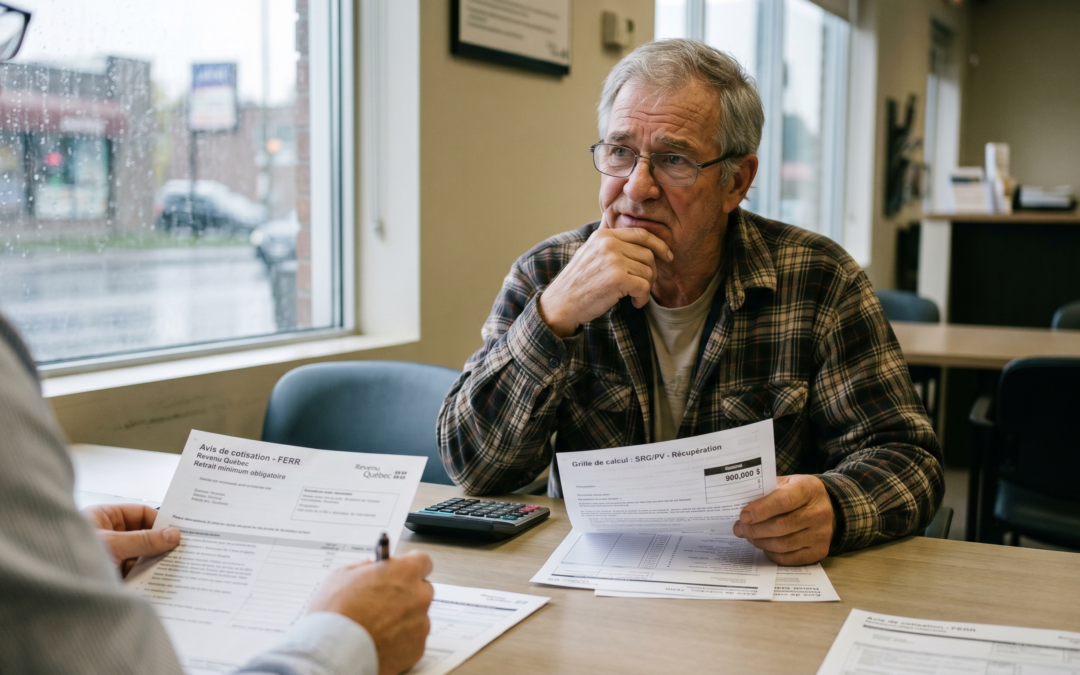

Take three Canadians in retirement. Brian lives in Hamilton, a former plant foreman, age 71. For forty years, he followed his branch manager’s advice to the letter: max out the RRSP, contribute religiously, never touch the capital before retirement. Today, his RRSP is worth $900,000, and Ottawa, like the Canada Revenue Agency, forces him to convert it into a RRIF. First mandatory minimum withdrawal at 71: 5.28 % of the balance, around $47,520, fully taxable.

Carl lives next door, in the same Hamilton neighborhood, a former security guard, also 71. He never contributed to an RRSP. He raised three kids on a modest salary and put practically nothing aside. He collects the Old Age Security pension, the full Guaranteed Income Supplement, the GST credit, and that’s about it. Reported income: near zero. Federal tax paid: zero.

Étienne lives in Forest Hill, Toronto, with a sister property in Westmount, Montreal. He inherited a portfolio in nine figures and an apartment building on Sherbrooke Street. He does not « work » in any sense that Brian would recognize. His income shows up as capital gains from carefully spaced dispositions, as dividends drawn, drop by drop, from a holding company, as withdrawals from a TFSA, maxed out every year since 2009, and, most importantly, as loans drawn against his portfolio at his private bank. Lifestyle of $500,000 a year. Real effective tax rate: around 15 %.

Three Canadians. Three Canadas. And Brian, in the middle, pays the highest effective rate of the three.

Canada’s tax apartheid in retirement

The word offends. Good. Canada’s retirement tax system was not designed. It was stacked. Layer upon layer, over sixty years, by a parade of Finance Ministers who each wanted to correct one particular unfairness without ever asking whether the sum of all the pieces held together. The result is a U-shaped mechanism: the poor pay nothing because we help them; the ultra-rich pay a very small share because we let them organize their income; and the upper-middle class takes the hit at the full marginal rate.

The trap has a technical name: the GIS clawback. The Guaranteed Income Supplement is a social assistance program for low-income seniors. Maximum 2026 for a single individual: about $13,318 per year, tax-free. But from the first dollar of income reported anywhere other than in OAS itself, Ottawa takes back 50 cents of GIS for every dollar earned. Fifty cents on the dollar. Harsher than the highest federal marginal income tax rate on the most stratospheric incomes in the country.

Brian’s RRIF withdrawal counts as taxable income. At $47,520 of mandatory annual withdrawal, his GIS is wiped out entirely. His OAS pension of $742.31 a month starts getting clawed back, too: 2026 threshold of $95,323 in net world income, at a rate of 15 cents on every dollar above. Carl, meanwhile, sees his GIS intact because he has nothing else to declare. Étienne organizes his income so that no taxable dollar ever crosses the critical thresholds.

Ontario, Quebec, and the patchwork in between

Here is where it gets even crueler, depending on where the retiree lives. The basic personal amounts vary wildly across the country. In Ontario in 2026, the provincial basic personal amount sits at $12,747. In British Columbia, $12,932. In Quebec, $18,952. And Alberta tops the list at $22,323, by far the most welcoming province in Canada for the first dollar of retirement income.

Brian in Ontario starts paying provincial tax at a taxable income of $12,747. His RRIF withdrawal of $47,520 puts him well above that floor. Brian’s twin brother Réjean lives in Laval, with the same RRSP balance and the same retirement story. Réjean enjoys a higher provincial basic personal amount, but Quebec’s marginal tax rates run higher than Ontario’s once you cross the threshold. The combined marginal rate for a Quebec retiree withdrawing $50,000 from an RRIF is around 37.12%, compared with roughly 29.65% in Ontario at an equivalent income. Réjean pays more provincial tax than Brian on identical RRIF withdrawals. Federal-provincial stacking is in the DNA of Canadian fiscalism. No one talks about it.

And then there is the GIS. The GIS is entirely federal. The 50-cent clawback per dollar of other income applies uniformly across the country. Neither Ontario, Quebec, nor Alberta has the power to soften it, tier it, or offset it. Brian loses his GIS the same way Réjean does. The two provinces simply add their own provincial tax rates on top, at different rates. The Canada that Carter envisaged in 1966, where a dollar is a dollar, is unrecognizable here.

The silence of the banks

No one, in any bank branch in the country, is eager to walk Brian through these mechanics. For a simple reason, financial and base: assets under management. As long as the $900,000 sits asleep in the bank’s RRSP, the bank collects its annual management fees, its mutual fund commissions, its stacked MERs. The day Brian pulls the money out to melt it down into a TFSA or a non-registered account managed elsewhere, the bank loses the margin.

Let us be clear about what we blame the banks for. The RRSP was not bad advice for Brian. For forty years, his contributions generated tax deductions at his marginal rate at the time, the money compounded, sheltered from tax, and that very mechanism is what let him hit $900,000. Without the RRSP, his final balance would probably be $500,000, maybe less. The vehicle delivered the goods.

The real grievance is elsewhere. The branch manager in the navy suit who advised Brian to contribute for forty years never sat him down at age 58 or 60 to build a decumulation plan with him. That second half of the work was never done. Strategically draining part of the RRSP between 60 and 65, during the lean years before OAS and before the forced RRIF conversion at 71. Spreading withdrawals so taxable income does not spike at the same time OAS starts to flow. Shifting amounts toward the TFSA and the non-registered account during the years when the marginal rate is still reasonable. That work, no commission-paid bank advisor ever offered to Brian on his own initiative.

That said, the responsibility does not stop at the banks. Section 146.3 of the Income Tax Act requires an RRSP-to-RRIF conversion at age 71. Schedule III of the Regulation sets the minimum withdrawal rate at 5.28 % at age 71, rising to 6.82 % at age 80, and reaching 20 % at age 95. Canadian and Quebec tax law together define taxable income in a way that fully includes RRIF withdrawals but fully excludes TFSA withdrawals. The legislator wrote the trap. The bank merely chose not to explain it to Brian.

The other end of the spectrum: why Étienne pays so little

Étienne does not need a banker to figure things out. He has a tax lawyer, sometimes two, and a Bay Street accounting firm that prepares his annual plan. Let’s be honest: Étienne pays tax. More than Brian in absolute dollars, if only because his income is higher. But his effective tax rate is tiny relative to his wealth. That is where the unfairness lives, and that is where the mechanics get interesting.

First, the holding company. Étienne does not hold his portfolio personally. He holds it through a Canadian-controlled private corporation that pays corporate tax on investment income at roughly 50% in Ontario, but recovers part of that tax via the Refundable Dividend Tax On Hand mechanism when it later pays dividends to Étienne. As long as Étienne pays himself nothing or very little, the tax remains suspended within the corporation. When he finally takes a dividend, he receives it as an eligible dividend, taxed at Ontario’s top combined marginal rate of 39.34% in 2026. Not zero. But still below the marginal rate on salary or RRIF withdrawals at the same bracket. And the tax deferral inside the holding company can run for decades. This is the classic lifeline of Canadian family capital for the past fifty years.

Next, the capital gains inclusion rate. Mark Carney canceled the Freeland reform in March 2025 that would have raised the rate to 66.67% on annual gains above $250,000. Result: in 2026, the inclusion rate stays at 50 % on all capital gains, no matter the amount. This is precisely the tax break that Kenneth Carter denounced back in 1966, and it is Étienne’s main tool. From $250,000 in realized gain, only $125,000 is added to taxable income. At his top combined marginal rate of 53.53% in Ontario, the real tax on the full gain works out to 26.76%. For Brian, withdrawing the same amount from his RRIF at a marginal rate near 37%, the tax bite comes in at 37%. Ten percentage points of spread. On dispositions repeated year after year, that compound.

Then the TFSA. Since 2009, Étienne has contributed the annual maximum, for a cumulative room of $102,000, and invested in high-growth equities. The account is now worth several hundred thousand. Withdrawals do not count as income, do not affect OAS, and do not affect anything. Tax-invisible money.

And then, the masterstroke Brian does not even know exists: borrowing against the portfolio. Étienne does not sell his shares to live on. He borrows against them at a preferential rate negotiated with his private bank and uses the loan proceeds to fund his lifestyle. A loan is not taxable income. No disposition, no capital gain triggered, no tax. The interest on the loan, if contracted for investment purposes, becomes deductible to boot. At his death, his heirs will liquidate part of the portfolio, pay tax on the deemed disposition at death, repay the loan, and pocket the rest. Buy. Borrow. Die. Three words that capture fifty years of estate planning in Forest Hill, Westmount, and West Vancouver.

Taken together, these four mechanisms mean that an ultra-wealthy Canadian with a $500,000 lifestyle pays, in net effective terms, around 15 to 20% real tax. Meanwhile, Brian, with $50,000 in RRIF withdrawals plus OAS and CPP, hovers near 37%. There lies the unfairness. Not that the rich pay zero. But they pay, proportionally, far less than the man who spent forty years on a Hamilton steel mill assembly line.

And where does that leave us?

Brian has never heard of Kenneth Carter’s report. He never read a piece about the GIS clawback. He trusted. He ticked the boxes. He maximized his RRSP the way everyone told him to. And at 71, the state takes back, with one hand, the GIS he could have collected, and, with the other, the tax on RRIF withdrawals he never asked for. He will finish his days in comfortable middle-class retirement. Nobody is going to feel sorry for Brian. But the system he was sold did not deliver what it claimed.

Carl collects his monthly GIS cheque without asking questions, and lives just below the poverty line. Étienne signs off on his annual tax plan without asking questions, either, and lives very large.

A dollar earned by the sweat of your brow does not get taxed at the same rate as a dollar earned in the market or a dollar borrowed against a portfolio. Not in Canada. Not in Ontario. Not in Quebec either. And the con is that we keep telling Brian he made the right call.