News

My mission, to inform you!

“Money, if it doesn’t bring you happiness, it will at least help you to be miserable in comfort.”

– Helen Gurley Brown

“Start-Up” in Québec; sharpen your pencils, folks…

The conditions are more favorable for Quebec entrepreneurs in “Start-Up” mode to incorporate into another province. In addition, it is tax-efficient in many cases to diversify its active business income in cross-border provinces, such as Ontario and New Brunswick.

The “SBD“: Small Business Deduction

The ” SBD ” reduces the corporate tax rate granted to small and medium-sized businesses. You will understand that thisdeduction is very coveted by business owners; the tax reduction can be up to $ 95,000 for each associated group of Canadian-controlled private corporations ” CCPC. “

What’s the difference per se?

Specifically, in the province of Québec, since January 1, 2017, you have been at risk of losing $41,500 in tax savings related to the” SBD. “To prevent this predicament, you need a minimum of three employees who work 40 hours weekly, for a total of 5500 hours. The reasoning is that Quebec has decided to harmonize with federal measures, while other provinces, such as Ontario, have not followed suit. As a result, “Start-Ups” in certain cross-border regions should look to diversify their active businessincome in a nearby province.

To this end, Olivier Brabant, Director of Taxation at HNA LLP, shares with us: “Indeed, the Ford government has decided not to harmonize with this federal measure in 2018. The increased accessibility to Ontario’s ” SBD ” in the last federal budget can create exciting tax planning for some clients who are not entitled to the ” SBD ” in Quebec.

Exciting tax credits in la ” Belle Province.“

In general, tax credits are more attractive in Quebec; an example is the Scientific Research & Experimental Development “SR&ED” tax credit. In turn, Quebec grants a credit of either 14%/30% for the contractual payment of entities and salaries in the context of an “SR&ED” grant.

“Quebec attributes interesting tax credits, but for a very profitable business. So, the company that has relatively little equipment and does little or no ” SR&ED, “it is interesting to transfer part of its production/business to Ontario, adds HNA LLP’s tax expert.

Undeniably, a Québec “Start-Up” will have several small claims for tax credits and subcontractors. Of course, tax credits are less attractive than a deduction such as the ” SBD. “In addition, in Quebec, you have a minimum threshold of $50,000 for the “SR&ED” amount: this same threshold does not exist in Ontario. On the other hand, it is advantageous for “Start-Ups” withseveral small “SR&ED” expenses to adopt a project from an Ontario permanent establishment.

Business owners, your “lifestyle” income: salary or dividend?

The final question that a business owner will whisper during a tax consultation: “how should I finance my “lifestyle”? We have noticed, year after year, theatrical dissemination of information that varies according to the professional vocation of the information provider. Our goal is to give you a simple analytical framework in a general context of integrated financial/tax planning, allowing you to make your own decisions.

“lifestyle” income

The concept of “lifestyle” income is the sum of all our contracts, obligations, and personal activities resulting from an exchange of a counterparty debited from our bank account. This concept should be used to optimize your shareholder compensation. Go to your bank account; use your bank’s propriety budget tool to determine the total amount of your monthly obligations.

” A Start-Up “

First, the incorporation of a company allows you to use the concept of a dividend. It is important to note that when we start a company – as part of a project involving business risk – liquidity is often thin and sometimes missing. Thus, for a new company in “Start-up” mode, it could be wise to pay, respecting a determined time horizon, an income mainly paid as a dividend.

Use your compass

First, identify your corporate tax rate as a numerical percentage. This tax rate remains an important planning tool; it will be a “marker” for establishing your salary policy.

An Overview

Taxed at a “low corporate rate.“

From the outset, determining a shareholder’s remuneration will depend on the general calculation of the benefit of payment, either in salary or dividend. On the other hand, in the context of a business with a “low corporate rate” and a shareholder with a high “lifestyle,” a dividend payment has a better chance of winning.

Moreover, the dividend advantage is amplified when: your “lifestyle” burn rate is lower, or you are in a “start-up.” Furthermore, the social charges will not be as large, which favors the maintenance of the dividend advantage.

Taxed at a “large corporate rate.“

On another note, regardless of your “lifestyle” burn rate, there may be an advantage to paying a salary when your business is taxed at the “large corporate rate.” Indeed, the latter tends to weigh, according to a specific spectrum, towards the distribution of a corporate salary.

Professionals with a “hybrid corporate rate.“

In Quebec, you lose some tax savings related to a tax deduction if your employees do not work, in total, a certain number of hours of work. A company with a “middle rate between the lowand large corporate rate” is the simplest case to analyze. The salary will be predominant during the analysis, and it would be advantageous for them to favor the payment of corporate compensation.

Texas Hold’em Poker: $4.86M tax-free

Jonathan Duhamel has made several significant moves during his poker career. One of the most beautiful moments; was when he won prestigious Texas Hold’em poker tournament in Las Vegas in 2010. At 23, for four months, he pocketed millions of dollars. In addition, during his career, he made net gains over a very long period.

Recently, the corridor of decisions from the Tax Court of Canada “C.C.I.” delivered, analogically from a Hollywood film, a spectacular final & farewell goodbye in the lustrous poker career of Jonathan Duhamel. Indeed, the coup de grace, worthy of a remarkable performance on Broadway, of an Oscar trophy: was to convince the tax court that his winnings, drawn from the game of poker, were tax-free.

The general rule

Lottery winnings, as well as winnings from games of chance, are generally exempt from tax; they do not constitute taxable income. However, there is one overarching nuance: the taxpayer must not operate a gambling business.

A gambling business exists if winnings can be attributed to its expertise and abilities. In addition, there must be an indication of a systematic search for gain. In general, we seek to make gains if we adopt a behavior worthy of a businessperson.

Poker, hobby, or business?

Poker has a personal aspect, so you must see if the activities are organized enough to build a business. CRA will consider the following factors to plan a decision: the organization of poker activities, risk reduction strategies, simple pleasure, profit-making intention to earn a living, number/frequency of bets, etc.

Notwithstanding the criteria mentioned above; I would like to ask you a question that implements our “C.S.A. Common SenseAbilities”: is it possible for a participant to win a tournament of the prestigious “WSOP” without behaving like a responsible businessperson without being compulsive in his training, without being organized and finally, without implementing systems of strategies?

In essence, the chances of a group of persons – like any of the characters from Trailer Park Boys – winning a “WSOP” tournament in Las Vegas is practically zero. Consequently, it would be pragmatic to believe that the success of a poker player at the “WSOP” tournaments would depend on the many behaviors/activities necessary to ensure a successful businessperson or enterprise, no?

“ We got out lawyered.“

I apologize for this platitude; however, it is applicable in the Duhamel case: “Money does not buy happiness, but it can certainly buy you a great team of lawyers.” Following thereading of case 2018-1782 (IT) G, we, laymen who are not lawyers, may wish to examine, question, and clarify the following behaviors/activities:

• First, Jonathan Duhamel creates a holding company with a specific intention; to mitigate and ensure tax optimizationof the PokerStars convention agreement. This agreement, signed in October 2010, doesn’t it demonstrate the clearintention of becoming a professional poker player? If so, how can we still acknowledge and make a case for his Poker activities being a hobby and not a business?

• Jonathan Duhamel has written an 18-chapter book describing many methods used to win at Poker. Previous journalistic statements were not admitted in court. Indeed, there is no guarantee that they are accurate, but the spirit of journalistic writings at the time cannot serve as a guide to evaluating a person’s actual behavior?

• Jonathan Duhamel’s credibility is not in question; he can do complicated calculations in his head, but he has forgotten everything for the rest. According to the information in the judgment, his semantic memory seems on the cutting edge. However, his immediate, short-term, and long-term memory are failing.

• CRA’s auditors, in this case, failed to request the relevantinformation for years before 2010.

In short, smile; could you show us your teeth? Also, don’t forget to raise your glass of champagne, Jonathan. We can’t wait to seeyour next act; Go Big, do a Netflix documentary highlighting your Poker career!

Journalists: Know the difference between tax avoidance and tax evasion

God knows, over the years, writers have poured lots of ink onethics in taxation. Despite this, in all the published information, we appear to have confused, deliberately or inadvertently, the difference between two critical concepts in tax ethics, those relating to tax avoidance & tax evasion.

Primo, the instincts of the human being, resist sharing with others. Sometimes, for some people, their strong sense of ownership – as described by Jean-Pierre Vidal – refrains themfrom fully adhering to the law, consequently preventing themfrom reducing the fair sharing of their taxes with the state. Indeed, some taxpayers will try to manipulate the law favorably with more aggressive/abusive methods, including those related to tax avoidance.

Secondo, fraud-related behavior is tax evasion. These behaviors do not help our society because they violate the advancement of our purpose, which is related to financing our ecosystems of moral and social democratic priorities. Essentially, it creates dislocations and income shortfalls in our society’s budget.

What is tax avoidance?

Canadian tax legislation established the two ethics concepts discussed in this piece. In the case of tax avoidance, it does not involve any fraud or concealment of the facts; there is nothing hidden. It implies that one orders one’s affairs by the letter of the tax law; our goal is to minimize the taxes paid.

However, some tax planning strategies become more challenging to digest in the eyes of the law; when a person is going to create or invent one or more series of operations that conform to a literal or grammatical interpretation of the law but not to the general spirit of the law. The purpose of the series of transactions is to amplify a tax advantage, enabling a new resurgence of tax savings.

The burden of proof is on our tax agencies; they must prove that there has been an overinterpretation of the spirit of the law. If this is the case, they will remove the abusive tax advantage; from the series of transactions that may have been invented to create a tax advantage.

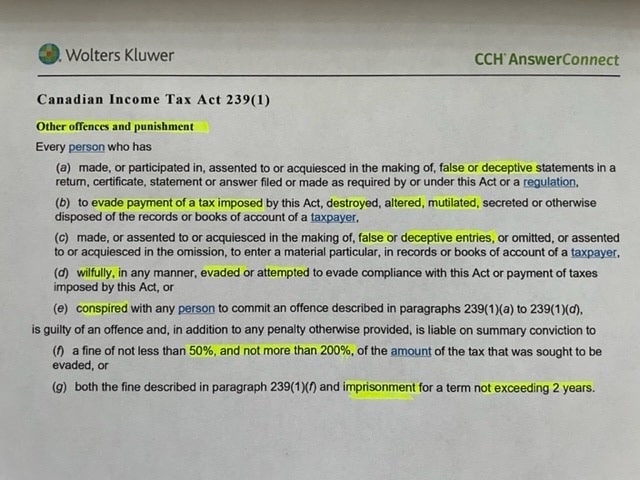

Tax evasion: prison?

Indeed, it is possible. Consider looking at the language used, by the legislator, in article 239 of the I.T.A. It’s not the language you will find anywhere else in our Canadian tax legislation; it’spowerful! Concerning tax evasion, we are in the criminal law sphere. It involves the concept of mens réa, a guilty, blameworthy spirit, and a deliberate intention not to comply with the law.

Examples of behavior related to tax evasion include and are notlimited to not filing your tax return, not declaring all your income, deducting non-existent expenses, adding personal expenses, falsifying information or documents, etc.

What is the common thread?

Countries that achieve their visions have strong social solidarity; this solidarity is relative, in part, to the acceptance of a balance of conflicting interests and, finally, of citizens who adhere to a fiscal culture to finance, in part, their society’s projects.

What constitutes the substance of this article is the loss of income for the state; the state needs resources to maintain our quality of life and ensure that Canada remains one of the best countries in the world.

Tax myth: Incorporation will lead to tax savings

First, some business owners will cross the Rubicon of incorporation sooner or later. The transformation from one legal personality to another is not without consequence: it is a crucial, irreversible choice that generates fundamental rights and obligations to be respected. With this in mind, we will discuss together the question of incorporation with the use of the following tags:

The concept of integration

Our tax system is based on the concept of integration. In a nutshell, the principle can be summarized as society’s tax fairness system. The more formal definition is one where the shareholder of a corporation will incur substantially the same combined tax burden as an individual who earns the same income.

For the most part, our system is almost perfectly integrated. However, believe it or not, in certain situations, the principle of integration can increase the business owner’s tax burden: “In certain circumstances, it could even cost him more […], according to Jimmy Lacoursière, tax specialist at Desjardins Wealth Management.

Tax savings

Contrary to popular belief, incorporation does not increase the accumulation of tax savings: “As for tax savings, this is probably the biggest myth associated with incorporation,” says the Desjardins tax expert. Consequently, there isn’t a Leprechaun with a pot of gold waiting to disseminate incorporation tax savings to our collective clients. The incorporation legend is only a tax legend!

Thus, the tax attributes surrounding incorporation have been primarily mitigated over time. At the same time, the budget tabled on February 27, 2018, by Finance Minister Bill Morneau has largely reduced the possibility of using its incorporation to economically diffuse retirement income to its shareholders.

However, as Jimmy Lacoursière confirms, incorporation will be preferred if the business owner cherishes other relevant and specific factors: “the evaluation must be done on a case-by-case basis according to different considerations […]. There are plenty of other good reasons to make incorporation relevant.”

Defer tax

A corporation’s tax deferral mechanism is effective if you can create excess liquidity in the corporation. In other words, if your lifestyle makes you consume all your business income, you lose one of the essential benefits of incorporation.

To this end, Jamie Golombek, CPA, CA, CFP, CLU, TEP, Managing Director, Tax & Estate Planning with CIBC Private Wealth in Toronto, adds a vital nuance: “The advantage is not really in the tax deferral itself but, rather, what may be done with the deferred amount.” So, unequivocally, excess liquidity can give you greater financial and tax planning flexibility. In addition, it can increase your quality of life.

Other relevant factors

As mentioned, the deferred amount is one significant advantage stemming from incorporation. However, we know that incorporation has many other benefits, including perpetual existence, limited liability, estate planning, division of ownership, financing, capital gains deduction, family trust, death tax reduction, etc.

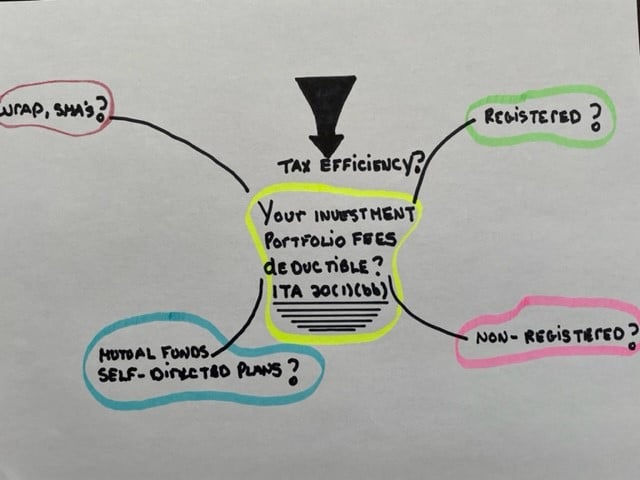

Your Investment Portfolio Fees: Deductible?

Your Investment Portfolio Fees: Deductible?

Fees paid to an investment advisor, counselor, mutual fund representative, or financial planner may be deductible. This deductibility increases the efficiency of your portfolio’s returns. However, fee deductibility is poorly understood in the financial services industry. Stay tuned for the following rules, as they will guide you towards the tax optimization of your portfolio.

First, fees must be paid to a person who is a financial professional. This person must devote themself primarily to providing advice on purchasing and selling securities and administering or managing an investment portfolio. You can only deduct fees; CRA will accept no commissions.

In addition, the concept of fees is defined in the tax law, and it is also cultivated as the following definition: « any means, which makes it possible to complete an exchange of services, directly or indirectly, received or to be accepted, to complete a series of specific operations. »

In other words, the management expense ratio (MER), which is the cost of managing your investment portfolio, is eligible for this deduction.

Registered plans

Registered plans are a tripartite contract between you, your financial institution, and the government. Fees that will be paid in a registered plan, including, but not limited to, RRSP, TFSA, RRIF, group RRSPs, and RPPs, are not deductible on your tax return.

Non-registered plans

Fees can be paid in several ways, and the tax impact will vary depending on the type of financial product you support in your account:

You use mutual funds.

Mutual funds are essentially investment trusts. In addition, mutual funds can be structured within a defined corporation, and they are called: corporate class funds. The trust, or corporation, manages its investments, and investors acquire units of interest within the specific business structure. These businesses are distinct, responsible, and in charge of the portfolio make-up and their particular investment policy statement. Unfortunately, you cannot deduct your fees using mutual funds or corporate class.

With that in mind, Michelle Munro, Senior Director, Retirement and Tax Research for Fidelity, explains why: « you don’t pay the fees directly, but instead, you pay a management expense ratio (MER). Mutual funds deduct the MER within the trust structure and make distributions after this deduction. »

In other words, your fees are already deducted for you inside the mutual fund. In addition, your accountant will be pleased to find that it is no longer necessary to indicate the fees on the tax information slips separately. Of course, you will save fees and time on your next tax return.

You are using an integrated account (WRAP) or a separate management account (SMA)

Holders of integrated or separately managed accounts pay their fees directly. You are the direct owner of the underlying assets, so you must report the gross income from your funds annually. This nuance is essential because it allows you to deduct the fees charged to your accounts as an expense.

In short, the investor’s net after-tax income will be identical whether you choose an investment trust, corporate class, an integrated account, or a separate management account.

Are there any tax advantages to choosing one account over another?

At first glance, there are several factors to consider, so it is a personal decision that will be made with your investment advisor. Undeniably, whether you choose a mutual fund or mutual funds within a corporate class structure, these are the most appropriate investment vehicles for most Canadian investors.

Finally, according to Ghislain Maillet, District Vice-President at Fidelity: « Fees are one of the biggest myths in the financial services industry. The reality is that investors have a choice: they can deduct all management fees directly or indirectly. Mutual funds are incorporated into trusts or corporations. In both cases, the fees are deducted at source (indirectly) before the net taxable distributions are passed on to investors. On the other hand, funds incorporated as corporations (class funds) offer real tax advantages such as converting foreign interest income and dividends towards taxation in the form of a capital gain (50% fewer taxes). »