News

My mission, to inform you!

“Money, if it doesn’t bring you happiness, it will at least help you to be miserable in comfort.”

– Helen Gurley Brown

Leaving Canada Without Leaving Your Taxes: Multiple Tax Mistakes Canadian Nomads Make (and How to Avoid Them)

- Factual resident: You live mostly in Canada, where you maintain significant ties

- Tax emigrant: You leave Canada permanently and cut your ties

- Non-resident: you live abroad and no longer have significant ties

- Deemed non-resident: a tax treaty gives you residency elsewhere

- Where is your permanent residence?

- Where is your center of vital interests (family, finances)?

- Where is your usual place to live?

- Nationality (as a last resort)

- Home in Canada

- Spouse or children in Canada

- Active bank accounts

- Credit cards

- Driver’s license

- Health insurance

- Clubs, associations, mailing address

- CPP/OAS: standard 25% withholding (often reduced per treaty)

- RRSP: 25% at source

- Rental income: 25% on gross (!)

- Election 216: being taxed on the rental net

- Form NR5: Reducing Withholding Tax

- Tax treaties: reduced rates depending on the country

- Visa or legal residency

- Accommodation

- Bank account

- Local ID card

- Tax Returns in the New Country

Brazil: a unified culture, contrasting tax realities

This article is part of the Tax Nomad® Service, a structured approach to taxation, developed to respond to an increasingly widespread reality: that of people and entrepreneurs whose lives, incomes and projects now go beyond the borders of a single country.

When leaving the airport in Brazil, the first thing that strikes you is neither the heat, nor the traffic, nor even the social contrast. It’s graffiti. Present everywhere, on walls, buildings, bridges, even on historic buildings, they instantly change our perception of urban space.

The paradox is real. By wanting to denounce a system perceived as unfair, some people are unwittingly contributing to weakening the esteem in which the city, culture, and even the country itself is held — a perception that takes hold from the outside as well as from the inside.

And yet, reducing Brazil to these visible signs would have missed the point. The creativity is immense: music, literature, cinema, humor, daily invention. The country lacks neither voice nor talent. And it is above all through words — and through language — that he expresses himself.

In Brazil, language is not just a tool of communication. It’s a cultural filter. Brazilian Portuguese largely dominates and, in the vast majority of cases, it is the only language really mastered. English and Spanish are not very present outside of tourist or corporate circles, despite the country’s position in Latin America. This is neither a flaw nor a weakness, but an assumed reality: Brazil has never adapted linguistically to its regional environment and has never felt the need to do so.

The consequence is simple but often underestimated. Living in Brazil without speaking Portuguese means living on the outskirts. You can stay there, consume there, observe. But to really integrate — understand the implicit codes, navigate the administration, establish lasting relationships — language becomes essential. The linguistic effort is not a comfort, but a mark of respect and the first gateway to real integration.

However, this common language does not imply a uniform population. There is no such thing as a “Brazilian face”. The country is the product of a profound mix: peoples, continents, cultures and histories fused into a new identity. Europeans, Africans, Aboriginals, Asians, Middle Easterners — everything has been juxtaposed, everything has been intertwined, everything has been transformed, everything has been reinvented. Brazil is not an addition of differences, but a culture born of all the others.

This diversity could lead one to believe that the country is fragmented. However, the Brazilian paradox lies elsewhere. Despite the immensity of the territory and the regional contrasts, a common culture runs through the country from one end to the other. From north to south, we find shared codes, a way of being and behaving in society that creates a surprisingly strong feeling of unity. Brazil is not a patchwork of juxtaposed cultures, but a cohesive collective identity, forged by mixing.

This contrasts with countries like Canada, where diversity relies more on the coexistence of distinct cultures, held together by a social contract of tolerance and institutional balance. Where Brazil absorbs and transforms, the Canadian model organizes and frames.

However, this cultural unity does not guarantee social equality.

In Brazil, the socio-economic disparity is visible and structural. The tax system is largely regressive. Consumption and essential services are heavily taxed, which places a disproportionate burden on the poorest households. Brazilians work a lot — often several jobs — for a return that remains low compared to the real cost of living.

In this context, certain practices are common and visible. Income splitting through the multiplication of legal entities is neither marginal nor hidden. It is a pragmatic adaptation to a system based on steep tax thresholds. Similarly, indirect taxes are usually integrated into the final price and not very visible on invoices, which reduces automated traceability and reinforces more targeted control, which is sometimes perceived as arbitrary. The system can be structured — it is when it operates internationally — but it is not uniform.

Taken as a whole, this framework creates a fiscal and financial disparity that can become advantageous for certain profiles. Effective rates are lower, the currency is weak, and monetary arbitrage mechanically increases purchasing power. These differences open the door to opportunistic but compliant taxation, provided that the rules, their limits and their evolution are understood.

Brazil also offers an attractive way of life: a life turned towards the outside, nature, energy, movement. But it would be dishonest to talk only about the advantages. Personal safety remains a real, manageable, but not theoretical issue. And the language remains a must: without Portuguese, we stay on the surface.

Becoming a tax nomad in Brazil is nevertheless realistic. Permanent residency is accessible through several routes — marriage, digital nomadism, retirement, entrepreneurship or investment — within administrative but predictable deadlines. It is not an improvised project, but a structural project.

In the end, Brazil is neither an automatic paradise nor a choice to be taken lightly. For the well-informed, prepared Tax Nomad® who respects the local culture, it can become a real place for living, business and freedom. But like all real freedom, it relies on understanding, structure, and execution.

Tax Nomad® guides individuals and entrepreneurs whose lives, incomes, and projects extend beyond the boundaries of a single country. The aim is to convert international mobility into a harmonious and legal tax structure.

Flow-Through Shares: A Powerful Yet Overlooked Tax Strategy for High-Income Investors

With Ontario’s top personal tax rate reaching 53.53%, high-income individuals are under growing pressure to maximize their after-tax returns. One underused but highly effective strategy is investing in flow-through shares — a mechanism that allows individual investors to claim resource exploration deductions initially incurred by Canadian exploration companies.

Let’s examine a simple example: an investor plans to withdraw $10,000 from their holding company for a personal investment. Depending on the form of extraction — salary, non-eligible dividend, or eligible dividend — the after-tax amount varies significantly.

After tax:

- A salary leaves $4,647;

- A non-eligible dividend provides $5,600;

- An eligible dividend yields $6,100.

If invested in flow-through shares, these amounts generate substantial tax deductions and credits — up to 53.53% in combined federal and provincial benefits — related to Canadian exploration or development expenses that the issuing company “flows through” to the investor.

Here’s the real advantage: the net cost to the investor after tax relief becomes:

- $2,159 with salary (only 21.6% of the original $10,000);

- $2,602 with non-eligible dividends (26.0%);

- $2,835 with eligible dividends (28.3%).

This means the investor could lose up to 70–75% of the value of the shares and still not incur a net loss — the tax benefit cushions the investment risk, effectively lowering the breakeven point.

⚠️ However, there is one critical planning mistake to avoid: do not use a Tax-Free Savings Account (TFSA) for this strategy. Flow-through tax deductions and credits apply only to taxable individuals. A TFSA is tax-exempt — it pays no tax and therefore has no taxable income to offset. This makes all the deductions and credits ineffective. In short, using a TFSA cancels the main fiscal advantage of flow-through shares.

The correct approach is to invest through a non-registered personal account, where the deductions can be fully applied to reduce personal taxable income.

To explore the full power of this strategy, Luc Dubé M.Tax (Tax Law Expert) and Jean Courcelles CFA, M.Sc (Investment Wealth Advisor) are hosting a free webinar: 🔗 Flow-Through Shares: Do Tax Incentives Provide a Sufficient Risk Premium?

This session is ideal for incorporated professionals, business owners, and high-income individuals seeking efficient ways to reduce taxes and enhance investment returns.

Old Age Pensions are out of control

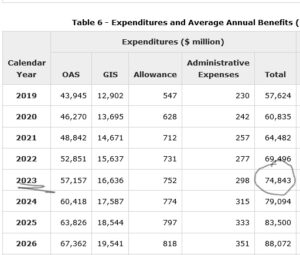

Concerning the 17th Actuarial Report, of the Office of the Superintendent of Financial Institutions (OSFI), there is every reason to believe that the estimated cost of distributing old age pension (OAP) cheque benefits will be $74 B in 2023. As we progress in time, the figures highlighted in the report will blow your mind: a creeping barrage of cost increases culminating at 116% in 20 years.

With that in mind, let’s take a few minutes to get used to the magnitude of these numbers. As eluded, this year, it is estimated that we will cash $ 74 B worth of OAS, GIS/Allowance checks; for comparison purposes, the projected cost of Highway 413 is around $ 10 B; so, it’s like buying the equivalent of 7-8 Highway 413 every year!

More surprisingly, in 20 years, the estimated cost of OAP is $ 161 B. In all these dimensions, the problem lies in the fact that our taxes pay for OAPs, so their net costs are a current federal government expense. In other words, we must pay the full spectrum of this bill without any contributory aid from our fellow citizens.

Moreover, starting from this premise, waiting 20 years before seeing the upward spiral of costs is unnecessary. In the same OSFI report, actuaries concluded that there would be a projected expenditure increase of 117% between the 2022 and 2023 years, a projected expenditure increase of $ 12.7 B for the period between 2022 and 2026, finally; The number of beneficiaries utilizing OAP will increase quite markedly.

By this very fact, the cause of the meteoric acceleration of this expenditure is, invariably, the change in our society’s demographic landscape. With that in mind, let’s immediately fix one thing with OAPs: their sustainability; their survival is at stake. But, above all, it is unlikely that we can improve and amend the program for future generations.

As per Statistics Canada website; on a webpage called population projections for Canada (2021 to 2068), we don’t need an in-depth demonstration of analysis to figure out that as our population grows, so will the need for OAP check benefits. Indeed, these stats aren’t meant to be projections; however, where there is smoke, you know the rest…

Case-in-point: glance at the age structure of the Canadian population; it is unequivocal. The population growth of Canadians aged 65 years and older will accelerate rapidly. The Baby Boom Generation will transition to, what I call, the Retirement Boom Generation. It is estimated that by 2030, in 7 years to be precise, the proportion of the total population aged 65 years and over will increase by an average of 22%. So, naturally, this will further exacerbate OAP costs and may lead to necessary tax increases for the sole purpose of the program’s sustainability.

We have been discussing the viability of OAPs for years, years, and years. But, as indicated, we may, this time, be at an inflection point. As you know, silly season is every 3-5 years; therefore, politicians will naturally try to kick this one down the road.

Every little bit counts when it comes to Health Care

In the end, statistics show that the number of Québécois who will be 75 years + in 20 years will completely explode, an increase of 79% (Calculation: CFFP; Source: ISQ). The results are surprising; consequently, we will have to change our tune to adjust our fiscal policy within 20 years, to better match this new demographic paradigm with the accountability of our public finances.

The rain of gratuity does not exist in tax policy; every dollar; every cent counts; We need to ensure that there is as little inconsistency as possible when it comes to tax fairness. In Québec, like the Scandinavian countries of Europe, we are progressive with our taxation policies. In other words, we are more inclined to use the power of our taxation measures for our people’s merits and goodwill.

Notwithstanding my last comment, and we must say so, no tax system can be perfect; There have always been flaws and illogicalities that hide in plain sight, in the cracks of the walls, encrusted, for a long time, in the fabric of our tax system. It goes without saying; it is inevitable.

In this sense, you will be surprised to learn, at least I was, that the wealthiest in our society can keep 40% of Quebec’s Family Allowances (the “QFA”). Specifically, QFA in 2022, including the supplement, for a couple with two children aged 3 and 7 is $5,228. QFA’s reduction parameters are approximately within the family salary range of $50,000, up to $110,000. Once you have exceeded this threshold, there is no more reduction, and you keep a floor amount of $ 2080.

Let’s go back to the same example, but this time, let’s evaluate the Canada Child Benefit (the “CCB”). On the Ottawa side, they are more generous; they allocate $ 13,994. The amount is reduced, even more so, from approximately $30,000, up to $70,000. Then, the reduction of CCB is linear to the wage upsurge, up to $ 200,000 of family income. Once you have crossed this amount, receiving CCBs is no longer possible.

Well, how do you explain these differences? In Québec, even if you are two doctors with children aged 3 to 7 and earn $1M together: we will still recognize that you have a greater capacity to pay taxes, so, in turn, we want you to keep the universality of QFA payment. I would go one step further: I’m speculating, but it is possible that we used the French tax system as a proxy to justify the allowance payment. This system enables us to obtain tax advantages by adding children to your family cohort.

Admittedly, at the federal level, the philosophy is significantly different. So, with that; even if you have two children and your family income is high; unless you have access to a childcare expense credit; You will pay the same tax with or without children in all high-income situations.

At this point in the story, it is imperative to address the elephant in the room: is it necessary to continue to give benefits to people who do not need them?

Yes, okay, you may be right: in short, only some families in Quebec with a family income greater than $200,000 and even fewer families with children of age for QFA. But, admittedly, when we multiply this number of families by the minimum floor benefit of $2,080, the amounts involved are relatively small and symbolic.

As mentioned at the beginning, there will be a meteoric increase in the number of people who will be 75+ years old within 20 years. So, why not abolish QFA for the wealthiest in our society and finally inject them into our health care system?

My dear politicians, if there is a matter that I guarantee you, the political issue in Québec, the sinews of war, lies in this “sandbox.”

When should you incorporate your business

Just the other day, Joel, a client of mine, a young real estate broker, asked me when he should incorporate himself. I gather that at first, he thought I would give him a cookie-cutter, easy answer. However, nothing is easy when transforming one legal personality to another; we must use caution and nuance.

From the outset, some business owners will cross the Rubicon of incorporation sooner or later. But, in Joel’s case, he didn’t expect it to come so soon. As you know, Canada’s real estate market has not stopped going gangbusters for the better part of the last 20 years. Moreover, Joel worked for his dad’s construction company, and things went well. He was earmarked to take over the company in 10 years.

The truth? He was miserable. He didn’t enjoy the daily grind of building houses and found himself daydreaming, wishing, and longing for a different path in life. Then, finally, a friend of his told him that he should explore the virtues of becoming a real estate broker:

« Joel, you would be perfect for that job; you know everything about houses.» Immediately, he had a « come to Jesus’s moment,» and this simple conversation sealed his fate. He found himself in real estate school the following month.

Here we are now, at this junction, where Joel is relatively prosperous and inquiring about incorporation. But, of course, many of his colleagues are incorporated and have told him: « Joel, it’s a goldmine; you will save tons of money.» When he told me this, I nearly choked drinking my coffee!

Then, he asked me:

« Luc, just give it to me straight, I made 300,000$ last year, and I’ll probably make more this year; should I incorporate? »

With his question in mind, I took out a piece of paper, grabbed my Sharpie fine point marker, and drew three circles: « Joel, for me to answer your question, we must first and foremost establish the true concept of incorporation without any of the tax myths. » Within every circle, I wrote down the following tags and preceded to explain the different concepts:

Tax integration: Our tax system is based on the concept of integration. In a nutshell, the principle can be summarized as society’s tax fairness system. Furthermore, there should be no difference in the amount of taxes paid between a person who is an employee and someone who’s incorporated and has their own business.

Tax savings: Contrary to popular belief, incorporation does not increase the accumulation of tax savings: « As for tax savings, Joel, this is probably the biggest myth associated with incorporation. Consequently, there isn’t a Leprechaun with a pot of gold waiting to disseminate incorporation tax savings. »

Defer tax: The incorporation mechanism is effective if you can create excess liquidity in your business. In other words, if your lifestyle makes you consume all your business income, you lose one of the essential benefits of incorporation.

In short, we ended the meeting with me explaining other relevant factors to be considered:

« Joel, take a few days and think about what we discussed today. Other relevant factors include perpetual existence, limited liability, estate planning, division of ownership, financing, capital gains deduction, family trust, and death tax reduction. »

Joel said he would follow up with me in a few days.