Leaving the country without dealing with it sometimes costs more than staying. The story of a retiree who thought he had everything in order.

Bernard Caron is 64 and spends eleven months a year in the tropics. A foreign residence card for seven years now. His Quebec health insurance card was handed back. No doctor, no spouse, no dependants in Canada. On paper, the man left the country long ago. Yet every spring, his accountant dutifully filed a Quebec resident return, worldwide income reported, as though Bernard had never moved.

Bernard thought becoming a non-resident was a decision to make someday. He was wrong. He already was one. Had been for years. He had simply never told the tax authorities, not in the proper form.

You Don’t Leave Canada in Silence

Let’s settle one thing right away. Tax residence is not a box to tick or a matter of which passport you hold. Since the Thomson decision of 1946, it is a question of fact. The tax authorities don’t look at your good intentions; they look at your ties. Spouse, dependants, available housing, health insurance card, driver’s license, bank accounts, subscriptions: every link weighs in the balance. As long as your life stays hooked here, you remain a resident. And every dollar of your worldwide income stays taxable in Canada.

Where It Hurts: The Apartment

What sinks these files almost always comes down to housing. A roof waiting for you, available at any moment, and the tax authorities conclude you never really left. Bernard had kept an apartment in Montreal “for appearances.” That is exactly the kind of detail that sinks a taxpayer. People have lost their case over a one-bedroom left empty, ready to take them back.

That said, his file held up. The apartment had been sublet under a real fourteen-month lease, dated and signed. The unit was no longer at his disposal. The lock gave way. Without that piece of paper, Bernard would have been pleading into the void.

The Return That Betrays You

Filing a resident return after you’ve left is clamping a wheel boot on your own file. Every slip signed as a resident contradicts the non-residence you claim. The auditor only has to throw them back in your face. The solution isn’t to defend the mistake; it’s to fix it. Voluntary disclosure. Correction. You set the record straight before the tax authorities get involved.

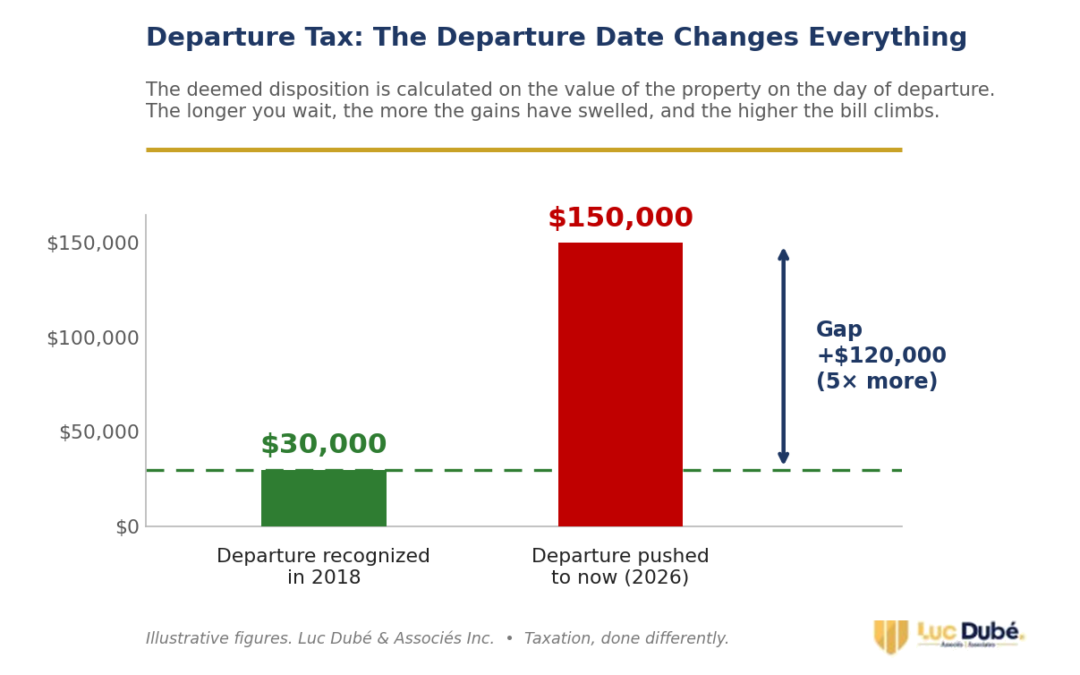

The Departure Tax Is Waiting

The day you stop being a resident, the tax authorities act as if you had sold nearly everything you own: investments, gold, crypto-assets, real estate abroad. This is the deemed disposition under section 128.1, the departure tax. The trap is in the timing. This tax is calculated on the value as of the day you left, not today’s value. Letting it drag on for ten years means risking tax on gains that have ballooned in the meantime, and having to reconstruct values from ten years ago from long-lost statements.

In Bernard’s case, setting things right today came to less than $45,000. Doing nothing and going on to defend a Canadian residence he no longer had would have cost close to $180,000. Carelessness has a price, and it is rarely modest.

No Treaty, No Safety Net

As for his host country, Canada has signed no tax treaty with it. No tie-breaker rule to catch him if two countries lay claim. Everything then rests on a factual break, black-and-white proof that his life is elsewhere. Residence card, physical presence, housing abroad, the RAMQ card handed back: a file like this is won with documents, not with oaths. When there is no net, you don’t walk the wire with your eyes closed.

What to Do, Concretely

First, set your departure date. Everything flows from it. Have your ties analyzed one by one before the auditor does it for you. Settle the fate of your home: sell it, rent it out long-term, or document that it is not at your disposal. Correct the returns filed in error rather than stacking them up. Calculate the departure tax on the right values, the ones from your departure. And report your foreign property, Form T1135 is not optional.

And You, Where Are You a Resident?

The worst file isn’t the one from the taxpayer who left long ago. It’s the one who let things drift. Who signed returns that contradict him? Who kept an apartment “just in case” and a vague tax status “to keep life simple.” The complication comes later, the day the tax authorities knock on the door.

A tax residence is documented before the audit, never during. That is the work of Luc Dubé & Associés Inc.: a residence analysis anchored in the facts and the case law, a departure date established, the departure tax calculated, the returns put back in order. Before the question becomes a problem.

If you’re unsure about your status, know one thing: the tax authorities won’t hesitate. Write to us at luc@lucdube.com.

Taxation, done differently.