The tax advantages of incorporation do not add up to a retirement. Some Financial Advisors sell a strategy called « Borrow, Buy and Hold ». Let us run the tax exercise, follow the money from age 45 to death, and see who really funds the retirement: the corporation or the annuity.

There is a sentence too many advisors still repeat to their professional clients: « Your corporation is your pension fund. » It is reassuring. It is simple. It is false.

A corporation has no retirement age. It draws no annuity. It leaves behind no surviving spouse. It is a tax-deferral and wealth-protection tool, nothing more.

Presenting incorporation as a retirement vehicle is not a matter of vocabulary. It is a technical error; the corporation never retires. Only the shareholder can.

Settle the principle up front. Canada’s tax-integration regime rests on a simple idea. Corporate and personal taxes, combined, should amount to roughly what the professional would have paid in salary for that income. The entrepreneur who pays himself an income pays substantially the same as an employee.

The tax advantage of incorporation comes down to one word: deferral. But deferral is not exemption. It is an interest-free loan the State always ends up calling back. Confuse the two, and you promise the client a pension that does not exist.

Mark Tessier, 45, and the pension he does not have

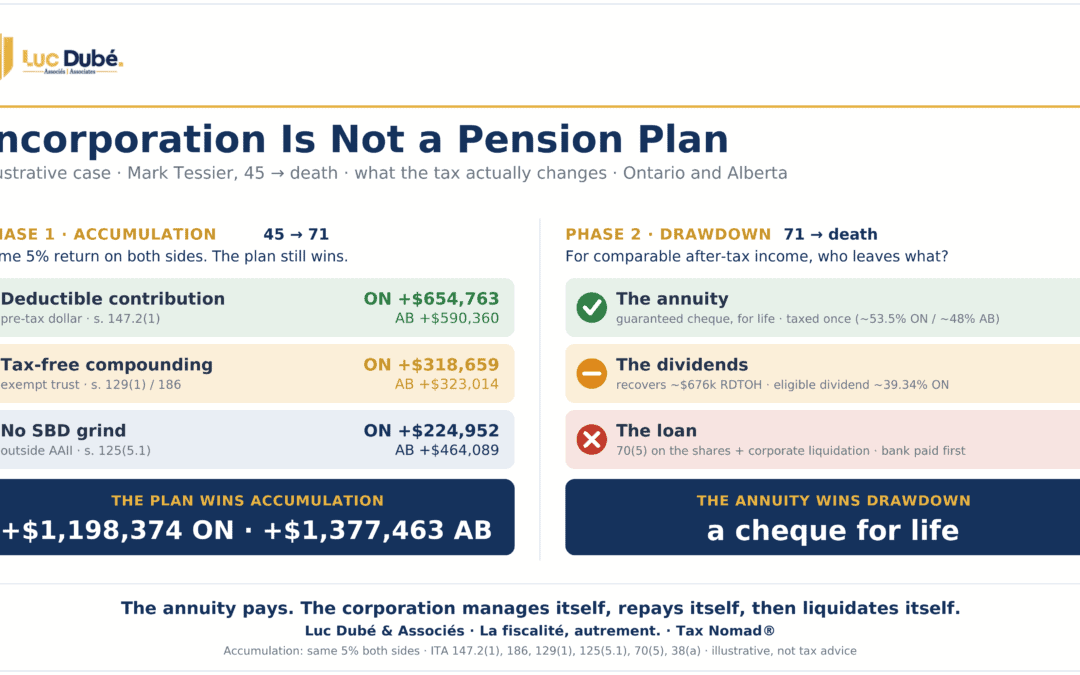

Take Mark Tessier. An illustrative case, but you meet dozens of him. A 45-year-old family-law lawyer in Ottawa, incorporated for about 10 years through an Ontario professional corporation. He argues separations, custody, support payments. He earns a good living. His corporation pays him a salary of roughly $196,600 in 2026, and year after year he has built up some $350,000 in his RRSP.

He has heard the sentence. His accountant, his advisor, his brother-in-law: every one of them swore his corporation was his retirement cushion. That all he had to do was let the money sleep in the company, invest it, pay himself later. Tax deferral as a lifeline.

But Mark is closing in on fifty, with no pension plan. Not a real one. He has a corporate balance, some investments, a maximized RRSP, and the comfortable illusion that all of it amounts to a pension. It is not a pension. It is a tax deferral dressed up as security.

The question before him is simple. Keep maximizing his RRSP, meaning $33,810 deductible in 2026, or let his corporation set up a registered pension plan built for professionals like him. The Income Tax Act, the « ITA », opens that door: a Personal Pension Plan, the « PPP ® », which brings together, under a single registered pension plan, a defined-benefit component and a defined-contribution component. And because Mark could just as easily hang his shingle in Calgary as in Ottawa, we run the numbers in both provinces, Ontario and Alberta, and let the statute speak.

One province, no hours test

Here is the first thing the sentence never mentions. Ontario asks no question about how many hours Mark works inside his corporation. No remunerated-hours test, none. His professional corporation is a Canadian-controlled private corporation, and its active income up to $500,000 qualifies for the small business deduction. In Ontario, that is a combined rate of 12.2%: 9% federal, 3.2% provincial. Move him to Alberta, and it is 11.0%: 9% federal, 2% provincial. Either way, the first half-million is taxed lightly, and the deferral looks generous.

That low rate is exactly what makes the illusion convincing. The money is barely taxed on the way in. What the sentence forgets is everything that happens next. Mark has an advisor. Registered with the Canadian Investment Regulatory Organization (CIRO), managing corporate accounts, with a dozen clients who look like Mark: doctors, dentists, lawyers, engineers, all incorporated, all sharing the same accountant. The strategy carries an English name that sounds good in a meeting: « Borrow, Buy and Hold. Borrow to buy securities, deduct the interest, then keep the securities without ever selling. The capital gain swells; the tax waits. In principle, nothing to object to. It is what comes next that goes off the rails.

Accumulation, and the balloon you inflate without seeing it

But there is a provision that never appears in bold on a slide: subsection 125(5.1) of the ITA. Warren Buffett said it best: it is only when the tide goes out that you find out who was swimming naked. In tax, that outgoing tide has a name. The reckoning. The moment you stop projecting and set the idea against two things that do not forgive: the text of the statute, which is not up for negotiation, and the real product, with its fees and its after-tax return, which rarely looks like the promise in the Excel table.

Since 2019, the rule on passive income inside a corporation is simple, and it bites. When a corporation collects passive income- portfolio dividends, interest, rents, the taxable half of its realized gains- that income inflates what the ITA calls « adjusted aggregate investment income », the « AAII ». As long as the AAII stays under $50,000 a year, nothing moves. At the first dollar above, the grind begins. Every excess dollar of passive income wipes out $5 of the $500,000 business limit. At $150,000 of AAII, the limit is zero. The small business deduction is gone.

And here the province decides everything, a point almost no one makes at the meeting.

In Ontario, the grind is only half a grind. Ontario does not follow the federal passive-income rules. When the federal limit melts away, only the six federal points go: the rate on that income climbs from 9% to 15% federally, while Ontario holds at 3.2%. Combined, 12.2% becomes 18.2%. Six points.

In Alberta, the grind is the whole grind. Alberta follows the federal rule to the letter. Both tiers fall at once: 9% to 15% federally, 2% to 8% provincially. Combined, 11.0% becomes 23.0%. Twelve points, double Ontario’s. Same strategy, same client, two very different costs, settled by nothing more than the province on the letterhead.

Why the PPP® Wins

Be fair to the illustration. Give both sides the same 5% return, the plan and the corporation alike, and strip out everything else. What is left is pure tax, and pure tax alone. The plan still wins.

Three weights explain why. The deduction, the yearly tax on collected income, the grind on the business limit: three weights, and every one lands on the corporation.

Then the tax on income collected. Reinvesting a dividend does not hide it from the taxman. The custodian issues a T5 every year, and the corporation reports the income regardless of whether it was reinvested. Inside the plan, none of this happens: the trust is exempt, and the return compounds untouched. Inside the company, the return is taxed year after year, and Part of it becomes refundable tax that sits on the books, earning nothing until a dividend is finally paid. Escaping that drag is worth about $318,659 in Ontario and $323,014 in Alberta.

Last, subsection 125(5.1) of the ITA itself. The plan’s capital lives in the pension trust, outside the corporation. It never enters the AAII, so it never touches the business limit. The corporate portfolio does the exact opposite: it feeds the balloon and grinds the deduction away. Dodging that grind is worth about $224,952 in Ontario and about $464,089 in Alberta, almost exactly double, because Alberta’s grind cuts twice as deep.

Add it up. The corporation started with the lighter tax on the way in and still finishes behind. In Ontario, by nearly $1.2 million. In Alberta, by nearly $1.4 million. Same 5% on both sides, no favor granted. The return that was supposed to rescue the corporation turned out to be a sword swung through water.

At 71, three roads

Accumulation is only half the story. The real test is drawdown, from 71 to death. Set one common target: comparable after-tax income each year so that the roads can be measured against each other. The match is never perfect. Different tax treatment means the three roads do not hand Mark the same net income to the dollar, and what each leaves at death should be read in that light—three of them.

The annuity. The plan converts to a life annuity, a cheque every month, for life, taxed once as income at Mark’s personal rate. The top marginal rate is roughly 53.5% in Ontario and roughly 48% in Alberta. Still, a life annuity is taxed across the brackets, so the average rate that actually bites is lower, closer to the high thirties in Ontario. It leaves no capital at death, because it was never a pile of capital. It was a paycheque that could not be outlived—no debt, no margin call, not one decision to make. The plan pays.

The dividends. Mark leaves the money in the company and withdraws it as dividends, one at a time. Each eligible dividend is taxed in his hands at an effective rate of about 39.34% in Ontario, which is lower than the 53.5% rate that applies to pension income. Here the refundable tax that slept for twenty-five years finally wakes: Subsection 129(1) of the ITA hands back 38.33 cents per dollar of eligible dividend paid.

But that pool is finite. It is an accumulated balance of roughly $676,000 at 71, drained inside about five years of distributions, and once it is gone no further refund comes. After that, the portfolio melts for good, taxed in Mark’s hands, and the shelter that made the road attractive is spent.

The loan. Nothing is sold. Mark borrows against the portfolio, deducts the interest under paragraph 20(1)(c) of the ITA, and lets the securities compound untouched. On paper, elegant. But look at who is lending: a bank facing a retiree with no income, holding the portfolio as collateral, charging a stiff rate while the debt swells quietly in the background. No personal tax, true. Not a cent. Until the day he dies.

Then the bill arrives all at once —and twice—first, the shares themselves. Subsection 70(5) of the ITA deems Mark to have disposed of his shares at fair market value the instant he dies, and that deemed sale triggers personal capital gains tax under paragraph 38(a) of the ITA. Nothing changed hands, yet the tax is real. Second, the portfolio inside the company.

To repay the bank, the estate has to sell. The securities are liquidated, years of untouched gains are realized in a single stroke, and the company is taxed on them. Here the capital dividend account splits the gain in two. The non-taxable half flows into the CDA and can be distributed to the estate as a tax-free capital dividend. The taxable half is not so lucky: it draws Part I tax inside the corporation, a slice of it refundable, sleeping on the books until a dividend releases it. One half walks out clean. The other pays.

And the bank does not wait its turn. A secured creditor is paid before the heirs see a dollar. Two tax layers, a loan to clear, a lender first in line: by the time the estate settles, it keeps a fraction of what the statement once showed. The road that seemed to leave the most leaves the least.

The reckoning, and the real question

Set the three side by side. The annuity leaves no capital, but it pays every month for life, with no debt, no margin call, not a single decision to make. The dividend road leaves something behind, after a lifetime of management and annual personal tax on the distributions. However, at the eligible dividend rate of near 39.34%, that bill is lower than the rate on pension income. The borrowing road leaves the least, after handing the portfolio to the bank and setting off a tax bomb at death.

Three thin estates, and a vast gulf in what each demanded along the way. On one side, a cheque. On the other, holding companies, rollovers, crystallizations, Subsection 110.6(1), Section 55, Section 84.1, Paragraph 20(1)(c), Subsection 70(5) of the ITA, fees that clear five figures without trying, possible margin calls, and the low hum of never being sure the right door was chosen.

So ask the question, the real one, the one no one puts to the client before selling him the structure: all this « rigmarole », is it worth it at the end?

The corporation is a fine deferral tool. It is not a pension. The annuity pays. The corporation manages itself, repays itself, then liquidates itself.