News

My mission, to inform you!

“Money, if it doesn’t bring you happiness, it will at least help you to be miserable in comfort.”

– Helen Gurley Brown

Property Tax Conundrum

Capital gains; for the rich?

Class warfare, which is as old as humanity, can prompt specific individuals to question the legitimacy of some of the fiscal tax advantages granted by our legislators. On this principle, the tax derogatory mechanism of the preferential treatment of capital gains (from now on, « PTCG ») is highly politicized because it involves an important social justice issue for our society.

Before even considering changing the parameters related to the tax expenditure of the PTCG, it is beneficial to know who will ultimately be affected/targeted by the change in its tax treatment. The people who have benefited from the PTCG last few years aren’t, in large part, the wealthiest in our society.

The target

Think about it for a few minutes; visualize your family and loved ones; I’m reasonably sure that you know people who have initiated, at some point, the following financial transactions:

First, they may have sold a home, afterward, disposed of shares on stock exchanges, then; sold a small business; finally, they may have used the deferral provision for capital gains (from now on, « CG »)

Considering the list of people you just made, is it fair to assume that all your loved ones are wealthy? Indeed. Contrary to popular belief, the longitudinal line of people who benefit from the PTCG is well-defined and balanced among the multiple social classes of our society.

The empirical example we have just made together is grounded and supported by statistics. The authors of the essay entitled « The Real Concentration of Capital Gains in Canada » dissected specific data banks and came to the following conclusion:

« Lower-income taxpayers benefit more than you might think from the PTCG, especially when they are 55 years of age and older[1].» (Underlined added)

Admittedly, taking a step back, it is necessary to go beyond the figures and ask questions. For example, the perception that capital gains favor the wealthiest in our society is linked to a historical statistical compilation problem. In other words, if the issue you want to identify isn’t adequately supported by the tax data compiled, invariably, our conclusions and perceptions will be wrong.

The clustering effect[2]

The starting point of this article is the actual and timely knowledge of the classes of people who benefit, in some way, from the PTCG. Naturally, the aggregation effect falsifies the data analysis, as there is a concentration issue of several sources of income in the highest income classification brackets.

To correctly specify the income classification of the people who are ultimately the users of the PTCG, it is imperative to create two classification categories; one class of people with total incomes that includes taxable capital gains (from now on,« TCG ») and the other, the new classification, subtracts the realization of TCG. This is because the latest statistical classification accounts for the TCG differently; it is embedded directly within the multiple income classes.

First and foremost, we note the concentration effect in the first ranking. Most of the total value of TCG[1] would be concentrated in the highest income class. The reason for the concentration effect in the first ranking is quite simple: when people lock in their TCGs, there is upward mobility in the scale of their total income. People in a specific class make more money, and there is an elevator effect.

In the new classification, when we exclude the realization of TCGs from the classification, there is a significant migration of the value of reported TCGs to the low-income classifications. More specifically, there is an economic trickle, even more so, in the class of people whose total incomes are less than $50,000. As a result, this classification has the highest percentage of the full value of the TCG achieved[2] among the five types of classes.

Table 1: CANADIAN TAX JOURNAL (2021) 69:4, 1193-1212, « The Real Concentration of Capital Gains in Canada », Authors: Tommy Gagné-Dubé, Matis Allali, Luc Godbout and Antoine Genest-Grégoire.

How can we explain this change? It is, among other things, a displacement of several million dollars and several thousand taxpayers to their respective and proper income classes without the clustering effect.

In short, the new classification gives us two key observations: first, low-wage taxpayers also benefit from the PTCG. Subsequently, it is essential to mitigate and nuance the perception that the more affluent taxpayers disproportionately benefit from the PTCG.

[1] CANADIAN TAX JOURNAL (2021) 69:4, 1193-1212, Authors: Tommy Gagné-Dubé, Matis Allali, Luc Godbout and Antoine Genest-Grégoire, p.1194.

[2] Id., p. 1196

[3] Id., p.1200

[4] Id.TABLE 1,p.1198

We are moving; where again?

As you are accustomed to every morning on the bridges, certainly you have noticed a fluid workforce and impressive interprovincial trade mobility between two Canadian cities. Indeed, the city of Gatineau, as well as the city of Ottawa, are, in large part, almost fully integrated economically. The two riverside cities are emblematic of a federal linguistic metaphor that connects two peoples, two cultures, in the same family ecosystem.

Certainly, even though it shares the same ecosystem, your quality of life can invariably differ depending on your province of choice. On the one hand, your quality of life may vary according to your province’s weight and tax burden; on the other, it will also depend on regional differences in real estate prices.

Considering your situation, which city/province can offer you a better quality of life?

Your tax expense

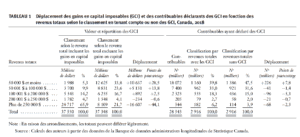

You would be surprised to learn that it is tax-efficient to move to Quebec. That said, according to the Research Chair in Taxation and Public Finance of the University of Sherbrooke: “The fact that the burden of personal income taxes is relatively high in Quebec is not necessarily indicative of families’ disposable income.”

Simply put, the weight of Quebec’s tax measures includes your taxes paid, and your payroll taxes, and we must subtract all benefits received from both levels of government. Quebec is more generous and distributes several benefits, such as the Québec family allowance. This has the effect of reducing the tax burden of certain Québec taxpayers.

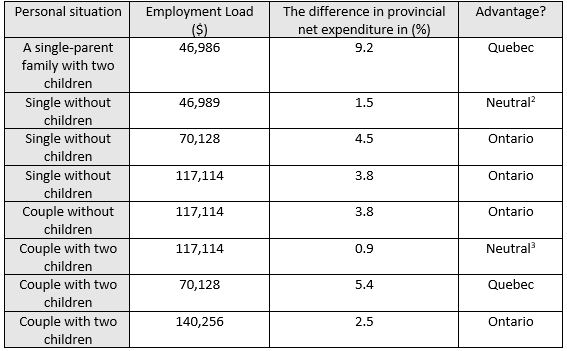

Here is a table summarizing several personal family situations based on your net tax expense. The gap is the differential between the burden of taxes on Canadian individuals.

However, as you have seen, a family’s average wages are relatively low. By broadening the average wage base, let alone making Ontario much more attractive regarding taxation. However, your tax expense is only one factor to consider in your decision-making: you must turn to the most important asset on your balance sheet.

Real estate

The highlight of the show for Québec is real estate. This component is not only important but also responsible, in part, for positive interprovincial immigration in recent years. On this principle, a single-family home in Ottawa costs an average of $606,300; the same house in Gatineau is $451,800. As you realize, the difference is considerable.

According to this same line of fire, a couple who buy this house will have different monthly payments depending on the province of residence. In this sense, the difference in monthly payments is approximately $997.

Of course, the choice of your province must be considered according to several criteria. Similarly, you must consider your family situation, average salary, and real estate preferences. Contrary to popular belief, moving to Quebec can be fiscally advantageous.

The elephant in the room

Québec purists will grind their teeth profusely with my following statement; in theory, you don’t have to learn French; however, in practice, you should be able to converse « en Français ». It would be best if you tried; it’s a question of respect. Consequently, you must remove the spider webs from Miss Culpepper’s « K12 French Books » at Woodroffe high in Ottawa. Remember, as Canadiens, our pluralistic society makes us different from our southern neighbors.

[1] Collective edited by Tommy Gagné-Dubé, Bilan de la fiscale au Québec – Édition 2023 (2023), Cahier de recherche 2023-02, Chaire de recherche en fiscale et en finances publiques, p. 85

[2-3] Table: the neutral position is because the gap is too small. It’s not enough to influence one way or the other.

[4] The mortgage comparison: $70,000 total deposit against mortgage loan; 5 years variable with static payments.

Dentist: « ITCs» in jeopardy?

In the Federal Court of Appeal « FCA » legal corridor, there is an appeal of paramount importance in indirect tax matters. The common thread of a specific fiscal ambiguity is now short-circuited to Dr. Kevin L. Davis, an orthodontist from the Greater Toronto Area. What is at stake for this dentist and his colleagues who are members of the Canadian Dental Association (from now on, « CDA ») cash flows of up to 35% of the estimated/realized value of orthodontic treatment.

The tax ambiguity in the Davis affair has to do with the qualification of the type of supply that needs to be used as per the Excise Tax Act (from now on, «law») as either a single or multiple supply. In a conventional orthodontics practice, multiple supplies may be eligible for input tax credits (from now on, « ITCs »). ITCs are monetary credits, in either GST/HST/QST, that your dental professional may receive due to an orthodontic service or purchases of appliance goods (from now on, “braces”).

Considering the historical context specific to dentists, how did we arrive at this cul-de-sac with the tax authorities?

The agreement

Legal ambiguities exist when dealing with multiple supplies, as it is difficult to determine the linkage to commercial activities which qualify ITCs entitlement. The law allows, in a different way, the two steps process necessary for conventional orthodontic treatment.

More specifically, the law states that ITCs are not eligible for an orthodontic medical service in one specific schedule. However, in another schedule, the law unequivocally states that purchasing orthodontic appliances such as braces is suitable for ITCs. When there are conflicting provisions of the law, we need to determine whether we can make them work together cohesively.

To bridge this gap, we witnessed in 1991 an administrative framework between CDA and the Canada Revenue Agency (from now on, “CRA”). The administrative arrangement stated that the two organizations agreed to reconcile the tax ambiguity. According to the passage of this agreement, ITCs are granted when the conditions of this framework are met.

Ultimately, the adhesion to the administrative arrangement framework directly benefits orthodontists where it counts (i.e., their wallets). There’s recognition and acknowledgment that orthodontists can make multiple supplies consisting of medical services and purchases of orthodontic braces.

As such, orthodontists must validate and identify each supply to properly acquiesce to the framework. Furthermore, the framework enables the orthodontist to file their GST/HST/QST returns using 35% of the total patient orthodontist treatment cost as consideration for the braces supply. In simple terms, orthodontists can further monetize the value of orthodontic treatment by squeezing and isolating the portion of refundable ITCs and those that are not.

Difference in opinion

The administrative framework, which is designed to bring unity and cohesion amongst two conflicting dispositions in the law, has undoubtedly created a difference of opinion between two tax agencies, Revenu Québec (from now on, (“RQ”) and CRA.

As for RQ’s position, it has always been the same, and has been for several years. Moreover, despite the administrative framework between ADC and the CRA, RQ has always believed that an orthodontic medical service and purchasing orthodontic braces are either an integral or incidental part of a single supply. According to RQ’s line of fire, dentists can’t claim ITCs on their single supply, as they are merely the continuation of a complete orthodontic single supply service.

A few years ago, CRA brainstormed, took a step back, rethought, and regrouped. The collective group thinking resulted in a complete overhaul of its multiple supply position. Acting back, the CRA reversed course and completely changed its tune. As a result, the CRA ultimately aligned itself with RQ’s position that a complete orthodontic service is indeed a single supply.

Similarly, CRA auditors began applying their new single supply position and theory across Canada. To achieve this, they sent notices of assessment to several CDA members; as a result, and as you can imagine, a panic set in in the dental community. RQ took a different approach and chose not to execute CRA’s newfound single supply position.

Indeed, a jurisprudential process is warranted to reconcile and qualify the type of supply dental professionals can employ in their practice. Consequently, how did we migrate toward this showdown in tax court?

The common thread

This trilogy began with Dr. James Singer, converging with Dr. Brian Hurd, and the final Court episode will be heard in the Dr. Kevin Davis affair. All these cases have the same common thread, that of the clarification, the qualification or not, of multiple supplies in the context of medical practice in orthodontics.

In the case of Dr. James Singer, he was a dentist who supplied artificial teeth. Multiple supply problems are inseparable from dentists who make and service artificial teething. In this case, Dr. Singer’s appeal was dismissed because he did not come to his hearing. However, Judge Bowman held, albeit in obiter dictum, that the Minister had erred in arguing that an artificial tooth treatment is ineligible for ITCs.

Yet, in the case of Dr. Brian Hurd, Judge Diane Campbell came to an opposite conclusion. According to her, braces and the orthodontic medical service must be combined and provided together. She concluded that we are dealing with a single supply framework that is not eligible for monetary refunds in ITCs.

Finally, this brings us to our case, that of Dr. Kevin Davis. First, Dr. Kevin Davis did not follow the administrative arrangement policy suggested by the CRA. This opened the door for CRA auditors, who, in turn, concluded that we were dealing with a single supply framework.

The judge, in this case, was Susan Wong, who ultimately rejected the Minister’s single supply argument. According to her, the law is unequivocal, clear, and precise. Moreover, it even added that it was futile to use and consider jurisprudential tests in this proceeding.

In short, until further notice, the administrative agreement framework is applicable and respected by the tax authorities. Dentists can adhere to the CRA’s administrative policy to claim ITAs on their complete orthodontic services. As eluded in my introduction, the decision is under appeal, and there can be a change in its administrative policy at any time.

“Flip $” your rental car

Are you looking to make a nice profit grab before the holiday season? You’d be surprised that your rental vehicle can get you back several thousand dollars. In some cases, it may be advantageous to buy back your lease, give your dealer a bank “draft” in an amount equivalent to the cash surrender value, and sell your vehicle on the Facebook marketplace.

A bargain to seize

From the outset, the market for new vehicles has been dramatically affected by the pandemic. Supply chains are slowing down, and as a result, automotive production remains anemic. In this sense, this appalling shortage has caused prices for new vehicles to skyrocket, but invariably, it has created great opportunities for those who sell or buy used cars.

In this vein, rental returns are a gold mine for dealers. In general, they repossess the rental vehicles at market conditions at the time and resell them, essentially, at a profit.

However, if it is appropriate for you to buy back your vehicle, you will have two choices. First, you sell to a person at the market price, and the other option is to keep possessing your used vehicle.

Facebook Marketplace

As a drop-off point, research and establish your property’s fair market value “FMV” if you opt for the resale of your used vehicle. This step is essential because the “FMV” of your car will be your reference point for accepting or refusing offers.

First, to buy back your leaser, you must give a certified cheque to your car dealer. Then, you are ready to make a “post” on the Facebook marketplace.

So, be prepared because car brokers will stick to you like “white on rice.” They are swift and aggressive, and their first offer will be ridiculous. Anchor yourself to your “FMV,” and you will see, like a “little gust of wind,” the increase in the pace of prices will follow the proverbial military step.

Replacement value

With that, it’s essential to calculate the replacement value, as it may be advantageous for you to keep your newly purchased vehicle from the dealership. Indeed, prices for new cars have increased by at least 20%-30% since the end of the pandemic. In addition, the financing needed to buy your property is also much more expensive.

Taxation

“Oh boy! ” don’t forget that if you sell your vehicle and make money, the tax man. Woman wants their cut. Our tax laws contain specific rules determining the tax consequences when trading on a “Property for Personal Use.” In general, notwithstanding the $1000 rule, the profit made on the sale of your car will be considered a capital gain, and 50% of your gain must be included in your income.

Entrepreneurs, are you pocketing the GST/QST difference?

Self-employed workers have the best of both worlds; they are mid-way between a

person who’s an individual, and a small business. Unfortunately, many self-employed

individuals don’t know that adherence to a GST/QST culture can result in a nice rebate

at the end of the year.

Beyond a certain income threshold, tax authorities require you to collect taxes on your

goods or services. However, your work as a “tax collector” can generate additional

business income since the tax you collect from your clients is not the same amount as

the portion you will have to return to the government.

Pocket the difference

Simply put, the tax collected from your customers is higher than all the taxes paid on

your deductible expenses. In other words, during your commercial activities, your

customers pay taxes. Then, based on Revenu Québec’s calculation method, you apply

the designated rate to your taxable income. Thus, your profit will be the difference

between the GST/QST versus the applicable Revenu Québec rate.

Heads or Tail?

An important decision you need to make is the method of calculation. There are two:

simplified and detailed methods for calculating your ITCs and ITRs. Self-employed

workers are generally businesses that primarily provide services. Therefore, consider the

simplified method for these types of companies; it will give you greater peace of mind.

Moreover, if your taxable sales are approximately $400,000 per year, including

GST/QST, you will probably have opted for a quarterly return; according to the Revenu

Québec website, the applicable rate is 3.6% for GST and 6.6% for QST.

Crunching the numbers

Your quarterly taxable supplies are 3.6% of $21000 and 6.6% of $21995. Added to this is

an additional credit of 1%. Your taxes to be remitted each quarter are $546 in GST and

$1,232 in QST.

Where is your profit? First, in GST, you collect 5% of your clients, but you only pay 3.6%

to Revenu Québec; The difference of $504 each quarter stays with your business. Then,

the same principle in QST; You receive $ 2194 from your customers, and you remit

1232$ to the Quebec tax authorities. In our example, an additional cash flow of

approximately 6000$ / year is added to your business income at the end of the year.

This is one of the rare occasions when you will be happy to pay taxes!