News

My mission, to inform you!

“Money, if it doesn’t bring you happiness, it will at least help you to be miserable in comfort.”

– Helen Gurley Brown

What If You Had One Last Chance?

Canada Turned Housing Into a Financial Asset. Now It Behaves Like One

A tax-free, leveraged bet on land has outcompeted productive investment and reshaped the economy.

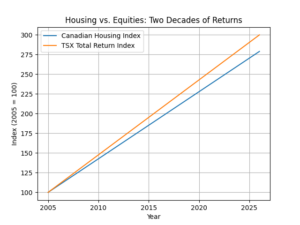

At first glance, the numbers tell a simple story: in 2005, the average Canadian home sold for approximately $230,000; by early 2026, that figure had climbed to roughly $660,000 (Canadian Real Estate Association, MLS® data). This is not merely appreciation; it reflects a deeper reallocation of how wealth is generated in Canada. Over nearly two decades, housing has delivered returns that resemble those of equity markets; however, the more uncomfortable truth is not that housing performed well, but that it was structurally positioned to do so.

That comparison, however, requires an important clarification: the TSX appears to outperform housing in Chart 1 because it reflects total returns, including reinvested dividends, whereas housing is measured primarily through price appreciation. A true price-to-price comparison significantly narrows the gap. The key takeaway, therefore, is not that stocks outperform housing but that housing, despite producing no income or economic output, has delivered returns comparable to those of equities.

As shown in Chart 1, while long-term performance may converge, the underlying drivers of those returns are fundamentally different, and it is precisely this difference that matters. A company grows because it produces goods, services, or innovation; a house appreciates because supply is constrained where demand is strongest, and because capital has been systematically directed toward it over time. Low interest rates, restrictive zoning, and demographic pressures all contribute to this dynamic; however, the most powerful force is fiscal. In Canada, housing is not merely an asset class; it is a tax-advantaged strategy.

At the center of this system sits a rarely debated policy lever: the principal residence exemption. In practical terms, it functions as follows: under the Income Tax Act, capital gains realized on the disposition of a qualifying principal residence may be fully exempt from taxation, subject to designation rules and conditions. While no explicit monetary cap applies, the exemption is limited to the designated number of years and restricted to one property per family unit. As a result, large gains can often be realized tax-free under the appropriate conditions. The Department of Finance estimates the annual fiscal cost of this measure at approximately $5 to $6 billion, making it one of the largest tax expenditures in Canada. Although politically sensitive and rarely reformed, the exemption has been indirectly constrained in recent years through measures such as anti-flipping rules and enhanced reporting requirements.

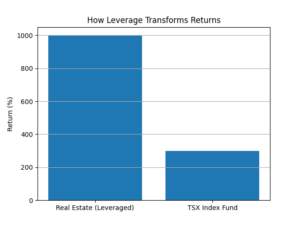

When combined with leverage, the effects are amplified dramatically: a $60,000 down payment on a $300,000 home in 2005 could now correspond to a property worth approximately $900,000, generating a $600,000 gain. This represents a tenfold return on invested capital, entirely sheltered from taxation under Canada’s principal residence rules. By contrast, an equivalent $60,000 investment in the TSX, with dividends reinvested, would have grown to approximately $170,000 to $230,000 over the same period, depending on market timing and return assumptions. These gains, unlike housing, would be partially taxable upon realization.

As illustrated in Chart 2, the amplification of gains, combined with tax-free treatment in Canada, helps explain why real estate has become a dominant wealth-building strategy for households. This is not a perfect apples-to-apples comparison, and that is precisely the point: while both real estate and equities can be leveraged, the nature of that leverage is fundamentally different. In housing, leverage is widely accessible, relatively low-cost, and supported by long-term financing structures such as mortgages, often with limited interim repricing risk. In contrast, leverage in equity markets typically involves margin borrowing or derivatives, which are more expensive, more volatile, and subject to margin calls, making them far less commonly used by households as a long-term strategy.

As a result, housing has evolved from shelter into strategy: over time, it has become a retirement plan, a primary wealth-building vehicle, and a leveraged investment structure embedded in household financial planning. The behavioral response is entirely rational: buy early, borrow as much as possible, and hold. This is not speculation; it is incentive alignment. Canadians did not collectively decide to treat housing like a stock; policy nudged them in that direction.

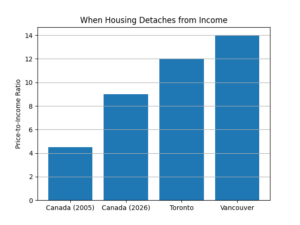

The consequences are now evident in the data: the median income in Canada was approximately $74,000 in 2023 (Statistics Canada), while the average home price now exceeds $660,000. This implies a national price-to-income ratio approaching nine, with major urban centers far exceeding that level (National Bank of Canada, Housing Affordability Monitor, 2025). Research from the OECD confirms that tax systems that fully exempt housing gains tend to distort capital allocation and contribute to upward pressure on prices (OECD, Housing Taxation in OECD Countries, 2022). Similarly, CMHC has noted that Canadian households are increasingly incentivized to rely on housing gains for wealth accumulation, reinforcing generational inequality (CMHC, Wealth and Generational Inequity in Canadian Housing).

As shown in Chart 3, this growing gap reflects structural affordability pressures and signals a market driven more by capital dynamics than by underlying income growth. This dynamic creates a self-reinforcing cycle: rising prices generate tax-free gains; those gains attract more capital; increased demand pushes prices higher still. The system feeds itself. This is not market dysfunction; it is the predictable outcome of the policy framework in place.

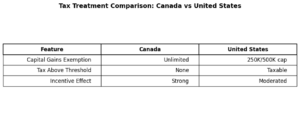

A comparison with the United States further clarifies Canada’s distinctive approach: under U.S. tax law, capital gains on a principal residence are taxable by default, though up to $250,000 for individuals and $500,000 for married couples can be excluded (Internal Revenue Code, 26 U.S.C. §§ 61, 1001, 121; Treasury Regulations §§ 1.121-1, 1.121-2). Any gain above these limits is taxed. This mechanism imposes a ceiling on tax-free accumulation and limits the extent to which housing can serve solely as an investment vehicle. Canada’s principal residence exemption, while subject to conditions, effectively allows qualifying gains to be realized tax-free, meaning the marginal dollar of gain can often escape taxation entirely.

As illustrated in Chart 4, Canada’s tax framework provides stronger encouragement for capital allocation into housing and contributes to higher price sensitivity. The broader implication extends beyond housing itself: when the most attractive investment in an economy is leveraged, tax-favored, and non-productive, capital will flow toward it. This means less capital directed toward businesses, innovation, and productivity, and more capital tied up in land and existing housing stock. Over time, this alters the structure of the economy itself. Canada increasingly risks becoming a place where wealth is built not by creating value, but by owning assets early.

For those who entered the market at the right time, the system has worked extraordinarily well; however, for new entrants, the equation is fundamentally different: higher prices, lower expected future returns, and increased exposure to interest rate fluctuations define today’s market. The question is no longer whether housing has behaved like a stock; it is whether Canada can sustain an economy in which the most reliable path to wealth has been ownership rather than production.

Ultimately, the conclusion is difficult to avoid: Canada did not stumble into a housing market that behaves like an equity market; it built one, through a combination of tax policy, financial leverage, and structural constraints. To realign housing with its intended social and economic role, policymakers, citizens, and industry leaders must actively reconsider these incentives and engage in substantive dialogue on reform. Unless these efforts are made, housing will continue to function not primarily as shelter, but as the country’s most powerful financial asset.

Disclaimer: This analysis is restricted to the principal residence regime under the Income Tax Act. It does not examine the tax implications applicable to real estate acquired or held for investment, rental, or business purposes.

Millennials & Gen Z Are Pissed Off: and Some Are Leaving Canada

A nation still wealthy on paper is confronting a growing generational fracture, where rising asset values have enriched the past while constraining the future.

The 2026 World Happiness Report delivers a result that should give policymakers pause. Canada now ranks 25th globally in overall life satisfaction, a notable decline from its 6th-place position a decade earlier. On the surface, this still places Canada among the world’s more prosperous and stable societies; by most conventional indicators, little appears fundamentally broken.

But averages can be deceptive.

Beneath the national ranking lies a far more revealing and troubling story. When the data is broken down by age, Canada no longer appears as a unified success; instead, it divides into two distinct realities.

Older Canadians are doing exceptionally well. Those over 60 rank among the happiest populations in the world, comfortably within the global top tier. Younger Canadians tell a different story. Individuals under 25 rank 71st, placing them below countries with significantly lower income levels and far fewer economic advantages. This is not merely a modest decline; it represents one of the steepest deteriorations recorded globally. Among 136 countries studied, only three have experienced a sharper drop in youth happiness than Canada: Malawi, Lebanon, and Afghanistan.

The comparison is striking. These are countries facing extreme poverty, prolonged instability, or armed conflict. Canada, by contrast, remains peaceful, affluent, and institutionally strong. Yet for its younger population, the lived experience is increasingly defined by frustration and diminished prospects.

The explanation for this divergence is not difficult to identify; it is largely rooted in the housing market.

For Canadians who entered the property market in the 1980s, 1990s, or early 2000s, real estate has generated extraordinary returns. Over time, rising home values have transformed ordinary homeowners into asset-rich households. Today, the median senior household holds net assets of approximately $1.1 million, much of which has been accumulated through passive appreciation.

Younger Canadians face a fundamentally different reality. Households led by individuals under 35 hold median assets closer to $159,000. This disparity is not the result of differences in effort or discipline; it reflects a structural transformation in how wealth is created and distributed.

Housing, once primarily a consumption good, has evolved into the central mechanism of wealth accumulation. The challenge is that the gains have already been realized. The same asset that generated significant returns for previous generations is now priced at levels that make entry increasingly difficult. Without a high income, substantial family support, or both, homeownership is becoming structurally inaccessible.

Labor market conditions further reinforce this imbalance. By late 2025, youth unemployment had reached approximately 14.7%. Nearly one million young Canadians were classified as NEET, meaning they were not in employment, education, or training. These figures point to more than temporary hardship; they signal a delay in economic participation with long-term implications for income, savings, and social mobility.

Importantly, this situation did not arise from a single policy failure. It is the cumulative outcome of a system shaped over decades. Zoning restrictions have constrained housing supply in high-demand areas; tax policy has made principal residences particularly advantageous; mortgage structures have encouraged leverage; and prolonged periods of low interest rates have driven asset prices higher.

Individually, each of these elements can be justified. Collectively, they have created a system that disproportionately rewards asset holders while raising barriers for new entrants.

The consequences are now visible not only in economic data, but also in behavior.

Younger Canadians are not simply frustrated; they are adapting. Some are delaying major life decisions, such as purchasing a home, starting a family, or committing to a long-term career. Others are looking beyond Canada altogether. The idea of leaving the country, once relatively marginal, is becoming increasingly common among skilled and mobile individuals.

This is not a dramatic or sudden exodus; it is a gradual and persistent outflow. It is driven not by crisis, but by comparison. Higher wages, more accessible housing relative to income, and stronger upward mobility in other countries are becoming difficult to ignore.

Canada, in this sense, is not failing in a conventional way. Its institutions remain stable; its economy continues to function. However, the balance that once defined it, a broadly accessible and resilient middle class, is beginning to erode.

The country still works; it simply no longer works equally for everyone.

Increasingly, younger Canadians are asking a straightforward question: if the system no longer works for them, why should they stay?

Article by Patrick Boyle & Transformed and Adapted for print by Luc Dubé. Based on the YouTube video: « Canada is a warning to the rest of the world.»

Spain: the rare balance between lifestyle, taxation and security

This article is part of the Nomadic Tax service®; the structured pragmatism of international taxation.

We had left Montreal for Paris on one of those transatlantic flights that have become almost commonplace due to frequency. This density of connections between the two metropolises is not anecdotal: it reduces the marginal cost of travel, makes professional mobility more fluid, and already prepares the mind for one of the cardinal ideas of contemporary nomadism: a world where certain distances cease to be obstacles and become simple organizational variables.

We spent a few days in Paris, which, let’s be honest, is an “open-air museum”. Then came the last segment of the trip: Spain. Two weeks. Valencia, Barcelona, Madrid y Sevilla. Four cities, four urban temperaments, the same feeling of intensity. However, during the first few days, the experience was more physiological than aesthetic. The jet lag weighed heavily. Sleep was disorganized, the biological clock was unravelling, and fatigue, far from dissipating, seemed, on the contrary, to thicken to the rhythm of connections, airport halls, and suitcases dragged from one terminal to another.

When we arrived in Valencia after an extra flight, we were exhausted, with migraines, and almost dazed. We dropped off our luggage at the apartment and then chose, without much thought, a small neighborhood cafeteria — a kind of rallying point for the regulars of the area. Inside, the room was full. People were talking loudly, laughing, drinking, and eating sandwiches on a long, loaf-like bread reminiscent of the French baguette. The atmosphere seemed strangely festive for a Tuesday morning. Without thinking too much, I headed to the fridge, had two local beers, and then came back to sit down.

I opened one.

My wife looked at me and said, with surprise mixed with disbelief, “What exactly are you doing?”

I almost pushed her away with a distracted gesture. I was tired, out of place, still trapped in the travel fog. She did not insist: she herself was in a similar state. I started drinking this beer like you swallow an improvised remedy, hoping to soothe the headache a little. Then, reflexively, I took out my phone to check my emails. And that’s when I saw the time.

9:04 a.m…. ?!?!?

I froze. I was sitting with a beer in my hand in a crowded establishment where, obviously, no one thought it was absurd to consume alcohol at nine in the morning.

This scene, as light as it may seem, sums up perhaps the spirit of this article better than any statistic. Spain is, first of all, confusing because of its pace. For a North American, it often gives the impression of a country that lives out of step with the clock. In reality, it lives above all according to a different logic of time.

There is nothing folkloric about the explanation. It is historical, social, and institutional. Spain has a unique relationship with the daily schedule: later meals, stretched sociability, long evenings, the centrality of lunch, and the density of urban life at the end of the day. Added to this is a structural legacy that is rarely well understood outside Europe: Spain observes Central European time, although its geographic position would place it closer to the British time zone. This discrepancy between the clock and the sun pushes the social day towards the evening. At the same time, the organisation of work remains regulated, with an average of 40 hours per week per year, without imposing a uniform schedule, which allows the coexistence of continuous days and days cut according to the sector.

In other words, Spaniards do not necessarily work less: they work differently. For a long time, the country cultivated, and then modernized, a more flexible organization of the day, in which the centrality of the meal, the temperature, the economy of services, and the urban structure shaped the time lived. To an observer in a hurry, this may seem casual. For those who take the time to look, it is rather a question of another social grammar.

This grammar is part of a remarkably powerful setting. Spain doesn’t just offer a pleasant climate or a generous table. It proposes a density of civilization. Its territory juxtaposes Roman heritage, Gothic monumentality, Andalusian layers, Mudejar refinements, Baroque brilliance, and modernist audacity. Between the verticality of the cathedrals, the golden stone of the historic centres, the dense grid of the old quarters, the proximity of the Mediterranean beaches and the possibility, in a few hours, of going from a political capital to a port city or an Andalusian landscape, Spain gives the rare feeling of a country where beauty is not exceptional: it is distributed. The traveller accesses it with disconcerting ease.

This quality of life could lead one to believe that Spain is characterized by economic slackness. This is the classic mistake. The numbers tell a different story. Spain has emerged from 2024 and 2025 with real macroeconomic strength. Its growth has remained solid, and its resilience is no statistical mirage. The country is not in retreat; On the contrary, it remains in a phase of dynamic consolidation.

But the Spanish singularity appears above all when we observe the composition of this wealth. Spain is one of the world’s great tourist powers. Tourism accounts for a considerable share of gross domestic product and employment. This point is fundamental: a substantial fraction of Spanish domestic demand is, in reality, supplied by non-residents. A visible part of the Spanish lifestyle — in the streets, restaurants, squares, shops, and infrastructure — is supported by foreign consumption.

The contrast with Canada is striking in this respect. Tourism plays a real economic role, but it has much less structuring power. The Canadian economy is more reliant on other drivers: resources, finance, real estate, utilities, and domestic consumption. In Spain, on the other hand, tourism, hospitality, catering, transport, and cultural services constitute a more visible, more diffuse, and more intimately integrated foundation into the productive fabric.

This does not mean that Spaniards live in a hedonistic parenthesis financed by others. Rather, it means that their economy, which is more tertiarized and more closely linked to international flows of visitors, distributes its hours, income, and uses of the city differently. The result is a country that seems less tense, less rigid, and sometimes more open to life, without being free of the demands of work.

For the tax nomad, this is where the analysis becomes particularly interesting. The question is not only: can we live well in Spain? The real question is: how is the relationship among quality of life, taxation, and security articulated?

In terms of personal security, Spain offers a reassuring profile for a Canadian resident. It appears to be a stable, accessible, and generally safe jurisdiction for travel and settlement. This reality obviously does not exempt us from a concrete reading of the neighbourhoods, lifestyle habits, and ordinary precautions, but it clearly contributes to the country’s overall attractiveness.

On the tax front, Spain and Canada have two distinct philosophies.

In Spain, the personal income tax is based on a conceptually essential distinction between the general base and the savings base. Income from work, employment, pension, or rental is subject to the general base and is taxed according to a combined State + Autonomous Community scale, which means that the tax burden varies significantly from one region to another. Madrid remains relatively more lenient; Catalonia is much heavier. For very high work-related incomes, the combined marginal rate may approach particularly high levels, depending on the Community concerned. Capital income, on the other hand, is subject to a scale specific to the basis of savings, distinct from the general scale.

Canada, on the other hand, juxtaposes federal and provincial taxes. The crude comparison of the top marginal rates between some Canadian provinces and some Spanish regions can sometimes yield results that appear comparable. However, the overall logic differs. The Canadian system is characterized by partial integration of dividends, specific tax credits, and separate treatment of capital gains. In many cases, it can thus offer a more favourable reading of capital income and a relatively more tempered pressure on certain categories of middle-class taxpayers. The Spanish system, on the other hand, is distinguished by a much more marked regionalisation and by a clearer separation between ordinary income and income from property.

In other words, Spain is not a simplistic tax haven. It can become financially attractive in specific scenarios, but it requires a detailed analysis of the residence, the source of income, the asset structure, and, above all, the Autonomous Community concerned. It is precisely for this reason that it constitutes a privileged field of analysis in any serious reflection on fiscal nomadism.

The question then becomes not only theoretical but also practical: how to legally settle in Spain?

The first and classic route is the non-lucrative residence visa. It allows you to reside in Spain without carrying out a paid professional activity. It is therefore suitable for people with sufficient passive income or assets that allow them to live without working locally. It is not a work permit and does not authorize telework. Eligible family members can obtain it with the holder, but this route is not, in itself, a gateway to a professional activity in Spain.

The second way, which is now the most emblematic in the logic of international mobility, is that of the visa, or the authorization for international teleworking, commonly known as the digital nomad visa. It is aimed at third-country nationals who wish to reside in Spain while carrying out a professional activity remotely for companies located outside Spanish territory, using exclusively IT and telecommunications tools. This is where one of its major attractions lies: eligible family members, including the spouse or equivalent, can submit their applications jointly or later, and family authorizations expressly entitle them to reside and work in Spain, both as employees and as self-employed workers. For a married couple who wish to transfer not only their residence, but also their real economic capacity, this point is considerable.

There are also other paths depending on the profile: titles linked to skilled employment, intra-company mobility, family reunification, or even certain ordinary residence regimes under common migration law. On the other hand, one point must be clearly emphasised: the so-called investor visa route has been abolished for new applications. Any strategy that presents Spain as still open to the golden visa for real estate or similar would now be an outdated reading of the applicable law.

It is precisely here, in my opinion, that serious reflection on Spain begins.

Spain must not be fantasized or caricatured. It is neither a basic tax haven nor a backdrop for an extended vacation. It is a dense, legally structured country, fiscally demanding in places, culturally splendid, economically resilient, and humanly habitable. It offers something rare: the possibility of a high compromise between intensity of life, personal security, urban sophistication, and legal international mobility.

For some taxpayers, Canada will remain more efficient. For others, Spain will appear to be a more complete destination — not only because people eat late, walk better, or live outside more, but because it sometimes allows them to align, in the same space, the residence, the couple, remote work, the beauty of everyday life, and an intelligible fiscal architecture.

This is undoubtedly the real lesson of this beer taken at 9:04 in the morning in Valencia.

It wasn’t just jet lag.

It was a brutal and almost comical entry into another way of inhabiting time.

🇨🇦 Equalization in 2026: A Quiet Shift That Could Benefit Ontario

Prime Minister Mark Carney’s recent remarks at Davos have crystallized a reality that policymakers and economists have increasingly acknowledged: the United States, long perceived as a pillar of economic stability, is now a growing source of political and economic uncertainty. By openly recognizing this shift on the global stage, Canada has positioned itself as a credible middle power, leveraging its natural resources, institutional stability, and diversified economic structure.

In this context, renewed global interest in Canadian resources, including energy, critical minerals, and strategic infrastructure, could support stronger-than-expected economic performance. However, this momentum is not evenly distributed across the country. Canada’s economic structure remains deeply asymmetric across provinces, inevitably producing both winners and laggards.

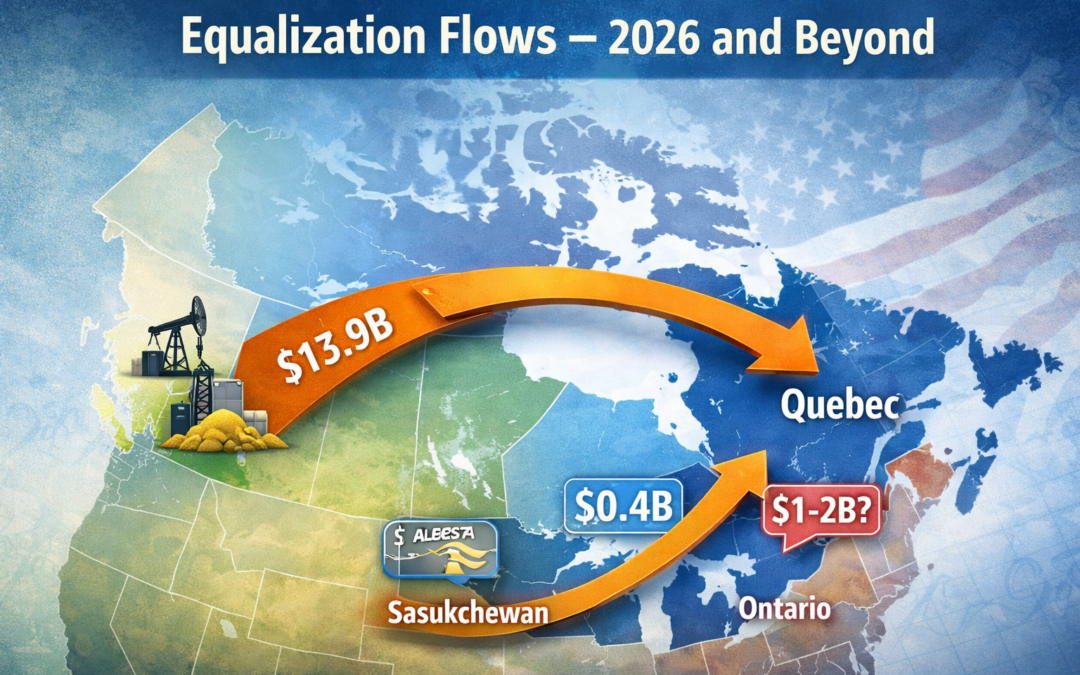

Historically, Quebec has been the dominant beneficiary of the federal equalization program. Yet recent data reveals a more nuanced picture. In 2025–2026, both Quebec ($13.6 billion) and Ontario ($546 million) received equalization payments; however, the scale remains vastly different. This pattern continues into 2026–2027, with Quebec projected to receive $13.9 billion, while Ontario receives $406 million.

At first glance, Ontario’s participation appears marginal. However, this static reading obscures a more dynamic and potentially consequential evolution.

In an environment shaped by asymmetric economic shocks, particularly the potential outperformance of resource-rich provinces and a relative slowdown in Ontario’s manufacturing sector, which remains heavily exposed to U.S. trade, accounting for roughly 75 to 80 percent of Canadian exports, a more pressing question emerges: could Ontario’s equalization payments increase materially in the coming years?

The institutional framework: a rules-based system

Equalization is not a discretionary transfer driven by political negotiations. It is anchored in section 36(2) of the Constitution Act, 1982, which commits the federal government to ensuring that provinces can provide reasonably comparable public services at reasonably comparable levels of taxation.

Payments are determined by a legislated formula based on relative per capita fiscal capacity across five major revenue categories: personal income taxes; corporate income taxes; consumption taxes; property taxes; and natural resource revenues.

Two technical mechanisms are particularly important: a three-year weighted moving average and a time lag of approximately two years. As a result, equalization payments in 2026–2027 reflect economic data from roughly 2022 to 2025.

The program is also constrained by a fixed overall envelope that grows in line with national GDP. This implies that increases in payments to one province must be offset by reductions elsewhere.

A static picture, a dynamic reality

Official projections for 2026–2027 suggest stability. Quebec’s payments increase modestly; Ontario’s remain limited. However, equalization is not a fixed entitlement. It is the outcome of a relative comparison across provinces.

A province does not receive equalization because it is weak in absolute terms, but because its fiscal capacity falls below the national average. Even modest changes in relative performance can therefore significantly alter entitlements.

The hypothesis: a relative shift in fiscal capacity

If resource-rich provinces benefit from sustained increases in energy and commodity revenues, the national average fiscal capacity will rise. At the same time, Ontario’s economy, still anchored in manufacturing and deeply integrated with the U.S. market, faces structural exposure to external shocks.

Under these conditions, Ontario’s fiscal capacity could decline further below the national benchmark, thereby increasing its entitlement to equalization payments.

The tipping point: Ontario’s re-entry into the system

Assuming a constant equalization envelope of approximately $27.2 billion, a material increase in Ontario’s payments would have direct redistribution effects.

At $1 billion, Ontario would remain a modest recipient; however, the shift would be structurally significant. At $2 billion, Ontario would become a more meaningful participant in the system.

In practical terms, a $1 billion allocation to Ontario could reduce Quebec’s payments by approximately $300 million; a $2 billion allocation could reduce Quebec’s share by up to $800 million.

A silent redistribution

Equalization adjustments are gradual, driven by averaging mechanisms and time lags. This creates a form of silent redistribution; politically understated, yet fiscally meaningful.

Why this matters for Ontario

For Ontario, the importance lies less in the magnitude of payments and more in what they signal: increased economic volatility; structural exposure to trade; and divergence in provincial growth models.

In this sense, equalization becomes a diagnostic indicator of economic performance rather than a simple transfer.

Conclusion: a shift worth watching

While Ontario’s equalization payments remain modest, the trajectory may be changing. If current trends persist, Ontario could see increasing transfers in the coming years, primarily at the expense of larger recipients such as Quebec.

Equalization is no longer just about redistribution. It is increasingly about relative positioning in a changing Canadian economy.

Can You Leave Canada and Pay 0% Tax?

Yes, It’s Possible: But It’s Not Magic.

Let’s clear the fog first.

It is possible to leave Canada and structure your affairs so that you pay little or no personal income tax.

But that outcome doesn’t come from hiding money offshore, burying crypto wallets in the backyard, or hiring a « creative » Tax Law professional.

It comes from understanding something very simple:

Canada taxes based on residency, not citizenship.

You can be a Canadian citizen and not be taxable under the Income Tax Act if you are no longer a tax resident of Canada.

That distinction matters.

Citizenship is political.

Tax residency is legal and factual.

If you properly cease Canadian tax residency, worldwide taxation under the Act stops. But departure tax rules, source rules, treaty rules, and corporate residence rules still apply.

Which brings us to what I call the three-part love triangle.

The Three-Part Love Triangle

Think of international tax planning like a love triangle.

You;

Your former country (Canada);

Your new country of residence;

And, if you’re a business owner, your corporation’s jurisdiction.

Four players. Three relationships. One complicated dynamic.

As with most love triangles, someone always wants more than they’re getting:

Canada doesn’t like breakups; it’s very jealous. Your new country wants commitment. Your company needs to live somewhere. Right?

If one relationship isn’t cleanly defined, the whole structure becomes unstable.

And like any messy triangle, it can get expensive. Case-in-point:

Leg 1: Leaving Canada: This Is Paramount.

If you don’t properly cease Canadian tax residency, nothing else matters.

Not Dubai.

Not Georgia.

Not Panama.

Not your Wyoming LLC.

Canada determines residency based on facts and ties. Not intentions. Not Instagram captions.

Primary ties:

- Home

- Spouse or common-law partner

- Dependants

Secondary ties:

- Bank accounts

- Provincial health coverage

- Driver’s licence

- Memberships

- Personal property

You must sever significant residential ties. You must file properly. You must address the departure tax. If you don’t?

The CRA may continue treating you as a resident. And if you are a resident, Canada taxes your worldwide income.

Clean exit first. Everything else second.

Leg 2: Choosing Your New Tax Home

Everyone must be tax resident somewhere.

You cannot float in fiscal outer space.

Some countries, like the UAE, impose no personal income tax. If living in a desert with a Camel pet, year-round sunshine floats your proverbial boat, Dubai may appeal to you.

Others, like Georgia, operate a territorial system. Foreign-source income may not be subject to local taxation. For opportunistic planners, that can look attractive.

Thailand? Two sets of rules: one presented neatly to international organizations such as OECD, and another that local practitioners navigate carefully. Remittance rules evolve. Interpretations shift. Administrative practice changes.

Here’s the risk most people ignore: Tax regimes change.

Governments revise remittance rules. Corporate tax appears where it didn’t before. Substance requirements tighten. Treaties are renegotiated.

When you build your life around a tax structure, you are betting that the structure won’t move.

It eventually moves.

And when it does, you must adapt.

Leg 3: Where Your Company Lives

If you’re a business owner, you must decide where your company resides.

Incorporation is not the only factor.

Corporate residence often depends on where central management and control are exercised.

If you move abroad but continue running the company from your Canadian condo that you «haven’t sold yet,» you may have a problem.

If you aren’t a business owner and instead live off retirement income, dividends, or investment gains, you must verify whether your new country taxes foreign income, and under what conditions.

Territorial tax regime does not automatically mean zero %:

Remittance-based systems can surprise you. Controlled foreign corporation rules can surprise you. Substance requirements can surprise you.

In a nutshell, that’s how it’s done.

But that’s not how it feels.

The Brutal Truth Most People Don’t Say

These structures are:

- Legal

- Used by normal professionals

- Often effective

But for how long?

The sum of all parts of the tax triangle requires:

- A very clean residency exit

- Proper corporate or investment structuring

- A banking strategy (increasingly difficult)

- Treaty analysis

- Exit tax modeling

- Ongoing monitoring

You still want the love triangle?

It may cost you more than Simon Leviev’s Tinder swindler scam.

Because this isn’t a one-time setup.

It’s an ongoing architecture.

And architecture requires maintenance.

Your Taxes Follow Your Life

Here’s something few advisors say clearly:

Your tax strategy must serve your Life. Not the other way around. If you design your life around avoiding tax, you may end up living somewhere you don’t want to be.

So, let’s flip the order:

Step 1: Start With Life, Not Tax

Instead of putting the cart before the horse, before obsessing over rates and jurisdictions, ask yourself:

What do I want?

To help yourself: Go to a wellness retreat if you must; do yoga; dance around a fire, and Journal for a week.

But answer this honestly:

- What kind of culture do I want?

- What language do I want to speak daily?

- What climate energizes me?

- How important is proximity to family?

- How important is safety?

- How important is infrastructure?

Your tax plan should follow your life goals.

Do not dictate them.

Sounds simple, right?

Most people skip this step entirely.

Step 2: Is Leaving Worth It?

Once you know what you want in life, then we can analyze whether leaving Canada makes sense.

Health.

Family.

Lifestyle.

Opportunity.

And last, yes, last, your bloody taxes.

Leaving Canada requires:

- Severing significant ties

- Filing departure returns

- Potential loss in paying departure tax

- Restructuring assets

- Possibly liquidating property

This is not a casual move.

If taxes are your only motivation, you may underestimate the trade-offs.

Step 3: Choose a Country That Fits Your Life

After doing the heavy lifting on your goals, choose a country that aligns with them, so you don’t get bored and return to Canada in 2–3 years.

There are incredible countries in the world:

Alive;

Fun;

Dynamic;

And, culturally rich.

You don’t have to live on « Survival Island » to lower some of your tax burden.

But remember, integration matters:

Learn the language;

Build community;

Understand the culture.

Otherwise, you risk becoming another quiet statistic, a Canadian who left for tax reasons and came back.

Step 4: The Rubber Meets the Road

Now we talk structure.

The more assets you have, the more options you have.

Generally speaking:

- Stronger currencies

- Higher personal security

- More developed economies

… often come at higher cost.

Let me give you a personal lens.

Brazil, for example, offers an incredible lifestyle. For some Canadians, purchasing power multiplies. Your dollar stretches. And yes, certain systems contain planning opportunities.

But trade-offs exist:

Security risks;

Infrastructure gaps;

And political volatility, although it exists everywhere now.

Panama and Costa Rica are generally safe. But safety often comes with higher real estate costs and higher cost of living,

There is no free lunch.

Step 5: Accept the Trade-Offs

Here is the uncomfortable truth.

Canada is one of the safest countries in the world.

Certain jurisdictions offer lower taxes but higher personal risk.

You may extend purchasing power fourfold, but you may also accept realities you never had to consider. You must consciously decide what you are willing to trade: Tax savings alone should not make that decision for you.

Final Thought

Can you leave Canada and pay 0% tax?

In narrow, properly structured scenarios: yes.

But the real question is not:

« Can I pay zero? »

The real question is:

« Can I design a life I genuinely want, and structure my residency and business around it in a legally defensible way? »

If you build your life first and your tax strategy second, the numbers may fall into place naturally.

If you chase the number first, you may find yourself booking a return flight home.

And that, ironically, is the most expensive outcome of all: Perhaps more than the « love triangle.»